MRM Research Roundup: Mid-October-2019 Edition

22 Min Read By MRM Staff

This edition of Modern Restaurant Management (MRM) magazine's Research Roundup features dismal restaurant sales traffic, best foodie cities , top breakfast foods in America, food fraud and why Brits love chicken shops.

Challenging Q3

The restaurant industry’s sales completed the gradual slowdown we’ve been witnessing since the beginning of the year and slipped into actual year-over-year contraction. For the first time in two years, growth was negative during the third quarter of 2019 with same-store sales growth of -0.4 percent (the first quarter of 2018 at -0.05 percent sales growth can be considered essentially flat). This update comes from Black Box Intelligence™ data from TDn2K™, based on weekly sales from over 31,000 locations representing 170+ brands and $72 billion in annual sales.

There was a bit of good news amid the otherwise disappointing quarter. The trend of two consecutive months with declining year-over-year sales reversed, with small positive same-store sales growth in September. Even more encouraging for the industry was the fact that September’s positive growth, albeit small at 0.1 percent, was achieved even though the industry was lapping over a month with relatively strong sales last year.

“This is something we were expecting given the underlying relentless erosion of guest counts and the fact that the industry was headed towards tougher previous year sales comparisons as we went into the second half of 2019,” said Victor Fernandez, vice president of insights and knowledge for TDn2K.

However, if we stand back and look at the industry from a longer-term perspective, things have not changed much. Same-store sales growth calculated over two years has remained positive the last four quarters. At 0.7 percent for the third quarter of 2019, it doesn’t show much of a decline from the average 0.8 percent recorded for the first three quarters of the year.”

Traffic Plummeted During Q3, Causing the Sales Stumble

Despite average guest checks growing at the same pace year over year for the last three quarters, same-store sales growth has been declining during each of those quarters. This is attributed to worsening same-store traffic growth. Same-store traffic growth in the third quarter was -3.5 percent, the worst result in the last two years and the only time guest counts declined by more than 3.0 percent during the same period.

Same-store traffic growth during September was -3.0 percent, which despite being a weak result, did represent a 0.8 percentage point improvement over the average results posted by the previous two months, providing further argument for September actually being a small recovery for a beleaguered restaurant industry.

Restaurant Sales Worsened By Hurricane Effect, Particularly In Florida

As predicted, restaurant sales suffered the effect of the massive storms hitting the southeastern part of the country during September. The hardest hit region was Florida, which experienced -3.1 percent same-store sales growth during September. Sales growth declined by 1.6 percent in that region compared with August, while every other region of the country experienced an improvement during September.

September’s same-store traffic growth in Florida was an abysmal -5.2 percent, which also represented a 1.6 percentage point drop from the previous month’s results.

Other regions affected by evacuations may have benefitted from the effect of severe weather, as people were displaced and forced to purchase more meals away from home within the same region but at more inland locations. The Southeast was the best performing region based on same-store sales growth during September as well as one of the top regions based on year over year sales growth improvement compared with August.

Fine Dining Still Winning the Sales Growth Game

Fine dining continues its dominance as the best performing segment in the industry based on same-store sales growth. This segment had the highest growth during the third quarter and also is the top performer year to date. Furthermore, if the trend holds through the end of the year it would be the third consecutive year of positive growth for dine dining.

The only other industry segment that was able to achieve positive same-store sales growth during the third quarter was family dining. This segment has been experiencing a resurgence lately, posting five consecutive quarters of positive growth, currently the longest streak of positive same-store sales growth by any restaurant segment.

However, it is important to note that the traffic loss problem is widespread throughout the industry. Note even these top-performing segments can escape from eroding guest counts. All segments experienced negative same-store sales growth during the third quarter of 2019.

Concerns for Restaurant Spending: Economic Uncertainty and Slow Income Growth

According to Joel Naroff, president of Naroff Economic Advisors and TDn2K economist, the outlook for the economy remains uncertain and dependent upon tariff actions. “The negative effects of the trade war are spreading across the economy, largely driven by business uncertainty. Manufacturing has already moved into a downturn. Job growth has slowed, due to businesses willing to leave job openings unfilled as well as the lowest unemployment rate in nearly fifty years limiting the supply of qualified workers. The result is that household incomes are growing more slowly, making it difficult for consumption to expand strongly. It looks like growth in the third quarter, which was just completed, will be in the 2.0 percent range.”

“Unless there is a breakthrough in the trade negotiations so that the threatened additional tariffs do not come into play, 2.0 percent growth might be the best we could see for quite a while. That is a warning that discretionary consumer spending, of which restaurants are a component, is likely to continue being soft going forward.”

Small Relief For Management Retention, But Staffing Still Concerning

Arguably, the two biggest headwinds faced by restaurants today are declining traffic and keeping restaurants staffed with enough qualified employees. TDn2K research shows there may be a lot of connection between the two. A recent study of restaurant brands achieving consistent positive traffic growth revealed these companies get much better guest sentiment scores based on their service according to White Box Social Intelligence™. They are also better at retaining their employees, particularly at the management level. Data indicates that those brands that get rewarded by incremental guest visits are perceived differently by their guests when it comes to service, and having a stable and engaged workforce is a great starting point.

Unfortunately for most restaurants, that is not the case. Turnover for hourly, non-management employees increased again during August and remains at historically high levels according to People Report. A large percentage of restaurants remain understaffed, especially in back-of-house positions, which have emerged as the largest pain point regarding staffing in restaurants.

There is a little bit of good news from the latest workforce results: restaurant management turnover decreased slightly during the latest month, an indication that increases may have plateaued. However, turnover for managers also remains at historically high levels and continues to be a concern, particularly because of the influence of management on hourly retention and engagement.

Looking Ahead

Same-store sales growth is expected to continue to be sluggish during the fourth quarter given the softening economic conditions and the fact that the fourth quarter of 2018 was the strongest in terms of same-store sales with 1.4 percent growth. Slightly negative sales, as seen during the third quarter, are likely to occur again in the last quarter of 2019.

Staffing woes are expected to continue. Historically high turnover for both hourly and management employees continues to be the norm and a large percentage of restaurants will continue to be understaffed as a result.

Data has shown that those companies investing in employee training, career development (particularly for their managers) and crafting a strong sense of purpose throughout their workforce will be those positioned to fare better in retaining and engaging their workforce. They will also provide a superior service experience to their guests, which ultimately is what wins the restaurant market share battle.

Best Foodie Cities in America

With Oct. 16 being World Food Day and restaurant prices rising 3.2 percent between July 2018 and July 2019, the personal-finance website WalletHub released its report on 2019’s Best Foodie Cities in America.

To determine the best and cheapest local foodie scenes, WalletHub compared more than 180 of the largest U.S. cities across 30 key metrics. The data set ranges from affordability and accessibility of high-quality restaurants to food festivals per capita to craft breweries and wineries per capita.

|

Top 20 Foodie Cities in America |

||

|

1. Portland, OR |

11. Orlando, FL |

|

|

2. New York, NY |

12. Sacramento, CA |

|

|

3. Miami, FL |

13. Tampa, FL |

|

|

4. San Francisco, CA |

14. Atlanta, GA |

|

|

5. Los Angeles, CA |

15. Denver, CO |

|

|

6. Las Vegas, NV |

16. Charleston, SC |

|

|

7. San Diego, CA |

17. Washington, DC |

|

|

8. Seattle, WA |

18. Honolulu, HI |

|

|

9. Chicago, IL |

19. Philadelphia, PA |

|

|

10. Austin, TX |

20. Oakland, CA |

|

Best vs. Worst

New York has the most gourmet specialty-food stores (per square root of population), 1.3655, which is 58.9 times more than in Pearl City, Hawaii, the city with the fewest at 0.0232. New York has the most restaurants (per square root of population), 7.50, which is 30 times more than in Peoria, Arizona, the city with the fewest at 0.25. Las Vegas has the most ice cream and frozen yogurt shops (per square root of population), 0.2955, which is 18.7 times more than in Lewiston, Maine, the city with the fewest at 0.0158. Santa Rosa, California, has the highest ratio of full-service restaurants to fast-food establishments, 1.80, which is 3.5 times higher than in Jackson, Mississippi, the city with the lowest at 0.51.

To view the full report, click here.

Harnessing Restaurant Technology

The National Restaurant Association, in partnership with Technomic, released its survey results on the state of technology and its impact on the off-premises channel in the restaurant industry. The study, "Harnessing Technology to Drive Off-Premises Sales," examines the key factors driving the growth of off-site consumption and explores how operators are using technology to drive and manage off-premises sales. The research, developed exclusively for the National Restaurant Association, is based on a study of a nationally representative sample of foodservice consumers and restaurant operators.

"The restaurant industry is constantly changing and technology's role in it continues to become more critical," said Hudson Riehle, Senior Vice President, Research and Knowledge Group, National Restaurant Association. "Now in our centennial year, we are seeing the industry change and adapt faster than ever before in response to the macro-environmental factors driving consumer behavior. In today's on-demand world, off-premises capabilities are more important than ever to keep restaurants aligned with the wants and needs of its customers. We're excited to continue to guide restaurants through these developments as we navigate the tech-forward future ahead."

As consumer lifestyles' are continuously driven by the convenience and speed of online and app-based ordering in other industries, approximately 60 percent of restaurant occasions are now off-premises across all forms, including drive-thru, takeout, and delivery. Customers are most receptive to consumer-facing technologies such as drive-thru enhancements, order accuracy tracking, and frictionless mobile ordering. Key areas of growth include:

- 92 percent of consumers use drive-thru at least once a month.

- 34 percent of consumers utilize delivery more often than a year ago.

- 79 percent of consumers use restaurant delivery (53 percent use third-party) at least once a month.

With 78 percent of restaurant operators considering off-premises programs a strategic priority, restaurant brands are investing big in technology, but are struggling to keep up with changing consumer expectations. Operators need to consider the increased standard of convenience in other industries and adapt accordingly when implementing off-premises solutions. Key investment statistics include:

- 74 percent of companies are investing in off-premises programs but none of the top 5 investments include customer-facing technology.

- 43 percent of delivery users place orders via restaurant apps while only 18 percent of operators offer mobile ordering via their own app.

- 66 percent of operators offer delivery through a third-party service and 55 percent offer delivery through internal staff.

The future of off-premises is far-reaching. Consumer receptiveness to enhanced restaurant technology extends both inside and outside the operation, and technology is becoming more commonplace. Key areas of emerging technology include:

- 22 percent of consumers used kiosk ordering last year and 11 percent used voice assistant ordering.

- If available, 69 percent of consumers would use vehicles with built-in heating trays to keep food warm and 41 percent would use autonomous delivery.

- 44 percent of restaurant operators who offer voice ordering, and 50 percent who offer location intelligence to target new customers based on their position, say it has a large positive impact on their business.

For further information on "Harnessing Technology to Drive Off-Premises Sales," click here.

Global Chained Consumer Foodservice Market

The latest study opines that the global chained consumer foodservice market is more popular than ever with paradigm changes in the way guests are eating and receiving their food. The chained consumer foodservice service market is expected to grow by around 4 percent over the forecast years, producing over US$ 280 Bn of incremental value from 2019 to 2027. This is partly driven by technology and mobile evolution – by digitizing the experience, consumers can get food whenever and wherever they like.

Growing investments in online food delivery applications is leveraging the global chained consumer foodservice market. Moreover, expenditure on quick service restaurants (QSRs) and hotels is increasing globally, which is expected to boost the growth of the chained consumer foodservice market during the forecast period.

Highly Individualized Eating Experiences and Increasing Number of Fast Food Kiosks in Favor of Market Growth

Increasing consumer awareness of quick-service restaurants is one of the key drivers expected to boost the chained consumer foodservice market's development in the coming years. With the increasing demand for fast food, there has been a substantial increase in the development of fast food chains, especially in markets of developing countries. Chained consumer foodservice competitors are beginning to adopt self-service kiosks which is achieving key objectives by not only improving speed of service but also enhancing cost-effectiveness.

The growing trend of socializing in cafes among urban millennials and youth is further fueling the growth of the chained consumer foodservice market. In addition, rapid infrastructure growth, including new airports and expressways in emerging economies, has also given scope to various coffee chains to set up their outlets. As a result, the growing inclination of consumers to consume fast food and other ready-to-eat (RTE) food items will enable fast-service restaurants within the chained consumer foodservice market to register a CAGR of close to 5 percent during the forecast period, 2019-2027.

Potential Product Shortages and Price Uncertainty May Continue to Halt Market Growth

Fluctuating food commodity prices are detrimental to the global chained consumer foodservice market. The shortage of raw material supplies may have a negative impact on the market during the forecast period. Shortages are mainly due to poor weather conditions and natural disasters which are expected to hinder the growth of the chained consumer foodservice market during the forecast period. Moreover, according to study analysis, paradigm shift has been noted in relation to the chained consumer foodservice market from the perspective of the masses. People are now preferring more nutritious, fat-free, and sugar-free products, and are usually more conscious about their health.

Stakeholders Invest Efforts in Reaching out to Varied Consumer Demographics

The chained consumer foodservice market is focused on businesses concentrating on providing product differentiation to satisfy the growing demand for nutritious food among customers. The chained consumer foodservice market seems to be moderately fragmented. The presence of a number of companies, including Brinker International Inc. and Compass Group PLC, makes the competitive environment quite intense. There are many overlapping and conflicting requirements from domestic regulators all over the globe. Different rules on allergens, trace components and pesticides have proved to be a hurdle for the global chained consumer foodservice market. Moreover, due to strong demand, location prices are expected to rise gradually, mostly within premium areas, thus offering more investment opportunities to the chained consumer foodservice market at the expense of independent players.

The study further offers a forecast of the global chained consumer foodservice market for the period 2019-2027. Considerable consumption trends of ready meals and on-the-go food products are leading to the development of the chained consumer foodservice market.

These insights are based on a report on Chained Consumer Foodservice Market by Persistence Market Research.

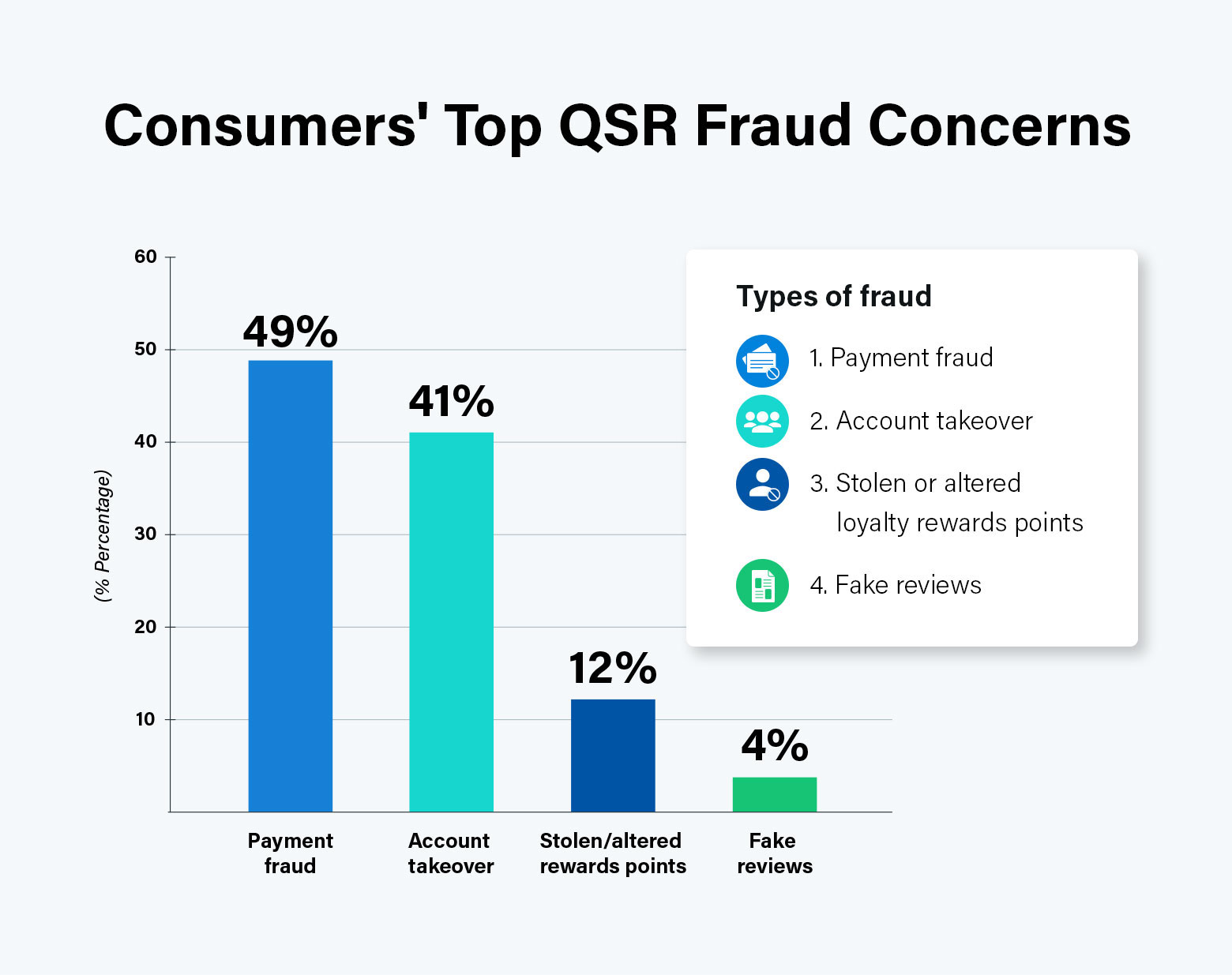

Food Fraud

According to Sift, consumer expectations for convenience have increased significantly across a variety of markets – and quick- service restaurants (QSRs) are no exception. Quite the opposite, in fact; recent reports show that about 33 percent of today’s dining experiences involve some type of smart device, making fast food even faster with pre-order options, in-house kiosks, and new services competing in the delivery space.

Yet the rise in these convenience-driven programs also introduce possible security gaps that put consumers at greater risk of fraud, which impacts customer satisfaction and long term loyalty. To dig deeper into the consumer perception of quick-service restaurant fraud, Sift surveyed consumers across the United States about their use of these services, their experiences with QSR mobile apps, and their concerns about fast food fraud.

Consumers want convenience, not complexity

It should come as no surprise that QSR customers expect experiences that are fast and seamless, with almost 40 percent of consumers reporting their number one frustration when ordering online and through mobile is experiencing a complicated login process and/or too many steps associated with accessing their account to place an order. But speed certainly doesn’t trump security–only 13 percent of survey respondents cited delayed order delivery as a factor when deciding to place future orders from the same QSR or third party delivery app. In fact, the survey found that con

consumers expect QSRs to prioritize security equal to their service-related demands. Here’s what we learned:

● Over half of survey respondents–62 percent–are concerned that their interactions with QSRs will lead to some type of fraud, whether it’s stolen payment information, account takeover, hijacked loyalty rewards points, or fake reviews.

● 49 percent are most concerned about their credit card data being stolen

● 41 percent are worried about account takeover, or ATO

To learn more, click here.

Early Bird v. Moonlight

The Jitjatjo team was running through some of shared some really counter-intuitive trends. They were even shocked by this data, but essentially after running numbers to determine where the majority of demand came for shift assistance from their clients, it turns out that morning prep work outweighs even the dinner rush.

Furthermore, they found Wednesday and Thursday are actually the best nights to pick up an extra shift. Data breakouts below as well as rates for various roles:

Table One: This analysis shows the overall split of our bookings across the period of a day.

Interesting that over 48% of these shifts are in the morning period.

Table Two: This analysis shows shift bookings across an average weekly period. Currently, Thursday is our peak day for business, with Wednesday not far behind, and overall a good mix across the week.

In terms of Categories and Rates, from our app, a sample of three Job Categories in New York, and equivalent rates:

Catering Server: $17.00 – $22.50

Dishwasher: $13.50 – $14.50

Line Cook: $16.00 – $18.00

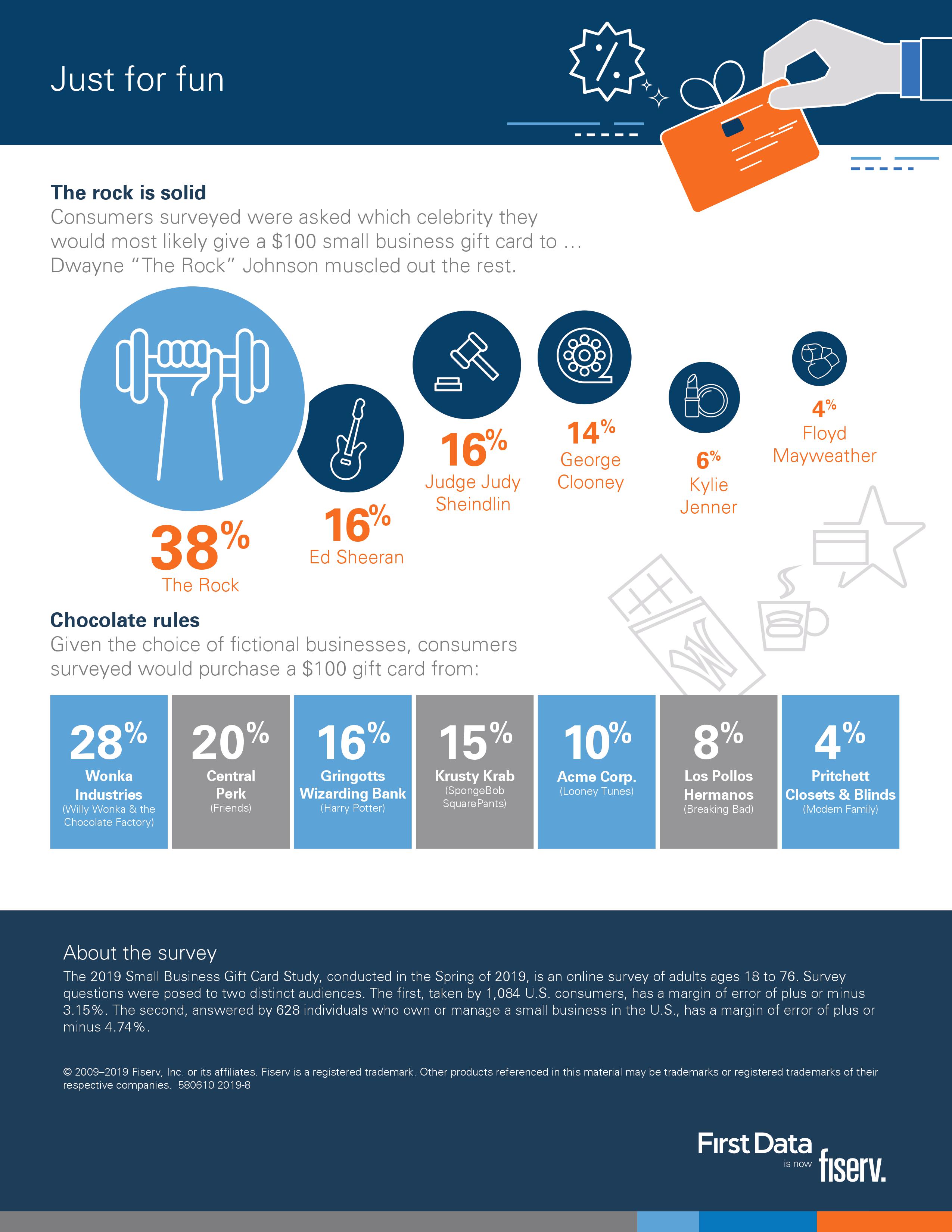

Gift Card Study

Eighty-eight cents may have more value than you think. According to the 2019 Small Business Gift Card Study, released today by Fiserv, small business owners can expect consumers holding a gift card worth less than a dollar to visit their store to redeem it. As small businesses jockey to increase foot traffic and engage customers in an increasingly competitive market, the study explores how consumers are using gift cards at small businesses, and highlights the benefits gift cards can deliver.

Conducted in the spring of 2019 and originally commissioned by First Data, now Fiserv, the study gathered insights from adults ages 18 to 76 across two distinct groups: 1,084 consumers, and 628 individuals who own or manage a small business in the U.S.

“Small business owners have a tremendous opportunity to boost revenue, foster customer loyalty, and strengthen their brand by investing in gift card programs,” said Dom Morea, senior vice president, Prepaid Solutions, Fiserv. “Gift cards are not only a potential growth engine for small business owners, they have become increasingly popular among consumers.”

Small Businesses, Big Benefits

Gift cards aren’t just for big businesses. In fact, 74 percent of consumers surveyed said they regularly buy gift cards from small businesses, underscoring that gift cards have utility at coffee shops and corner stores and that customers expect them to be available for purchase and redemption. The benefits of gift cards can be significant, helping small businesses attract new customers and build relationships with repeat shoppers. According to the study:

- 90 percent of consumers who receive a gift card from a small business they have never visited said they would shop at that business and return there in the future

- 56 percent of surveyed consumers join loyalty or frequent shopper programs at small businesses. The same group said gift cards are the preferred way for their loyalty to be rewarded

- Nearly four out of five consumers surveyed said if they have a gift card valued at 88 cents, they’ll visit the store to redeem it.

Whether Giving or Receiving, Dining Wins

Consumer opinions can vary widely, but when it came to determining which business types they’d most want to give or receive a gift card from, they tended to agree. The most desired business types for small business gift cards were, in order of popularity:

- Casual dining restaurants

- Coffee shops

- Specialty services (such as nail salons and barber shops)

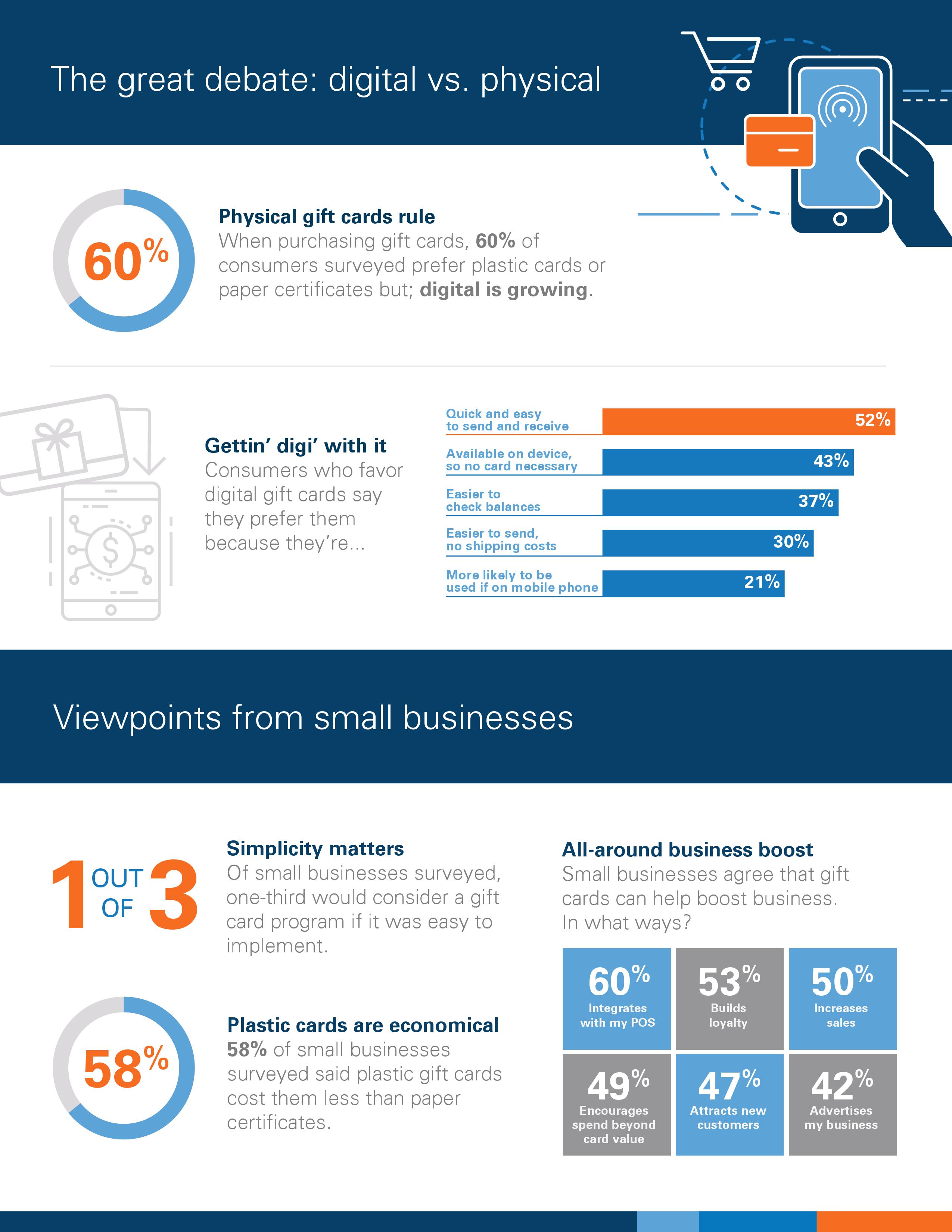

- Digital vs. Physical

While digital gift cards continue to grow in popularity, physical gift cards are still preferred amongst consumers. Of those surveyed, 60 percent said they prefer physical gift cards or paper certificates to digital versions.

Among the 40 percent of consumers who said they prefer a digital gift card, the main reason was because they are quick and easy to send and receive. Other benefits of digital cards are their availability on smart devices, and the ability to easily check the card balance.

Viewpoints from Small Businesses

Small business owners surveyed were clear that simplicity and efficiency of implementation and operations were critical elements to a successful gift card program:

The ability to integrate with a point-of-sale platform, such as Clover®, a cloud-based point-of-sale solution from Fiserv, was the top benefit to small businesses

One-third of businesses without a gift card option would add one if they thought it was easy to implement.

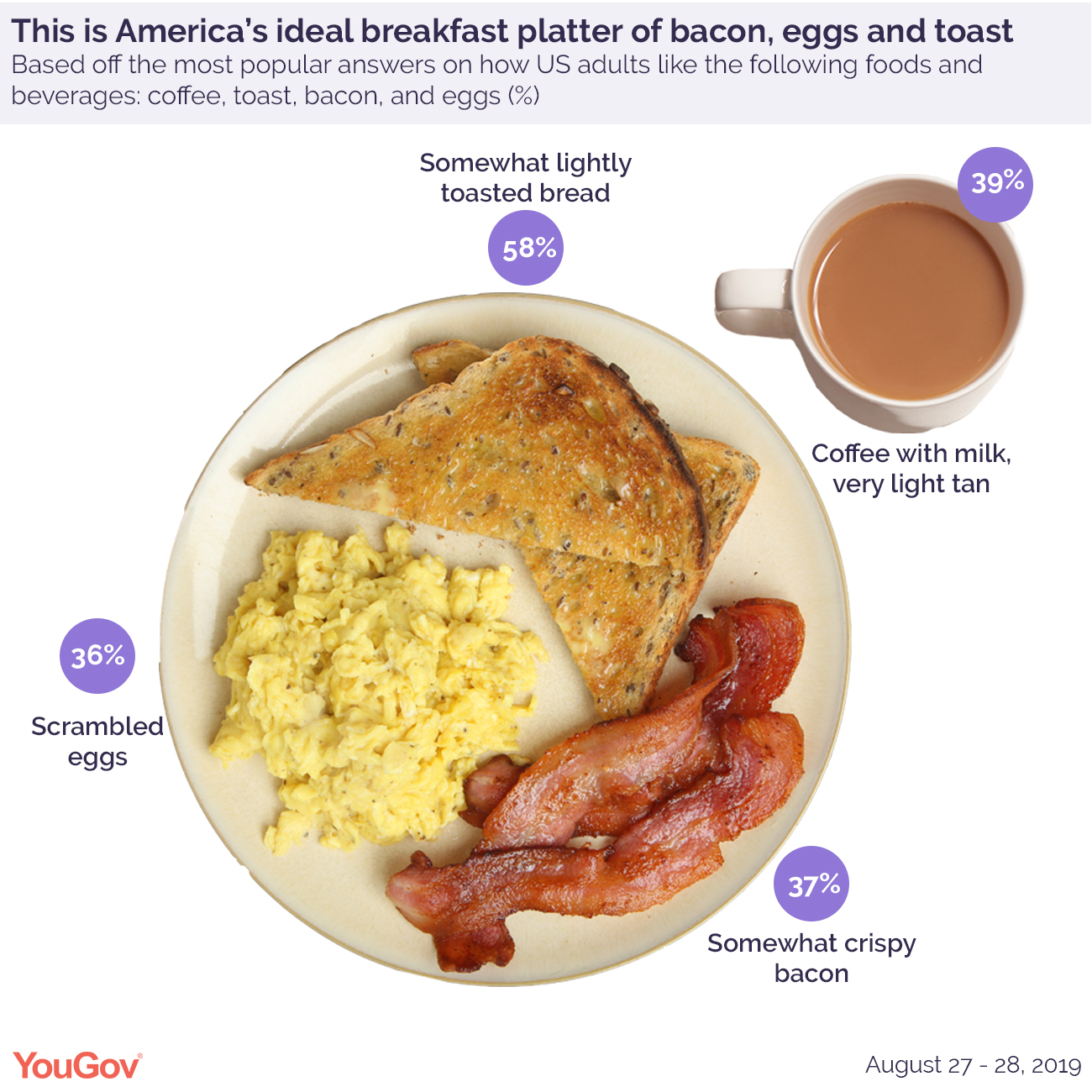

America's Favorite Breakfast Foods

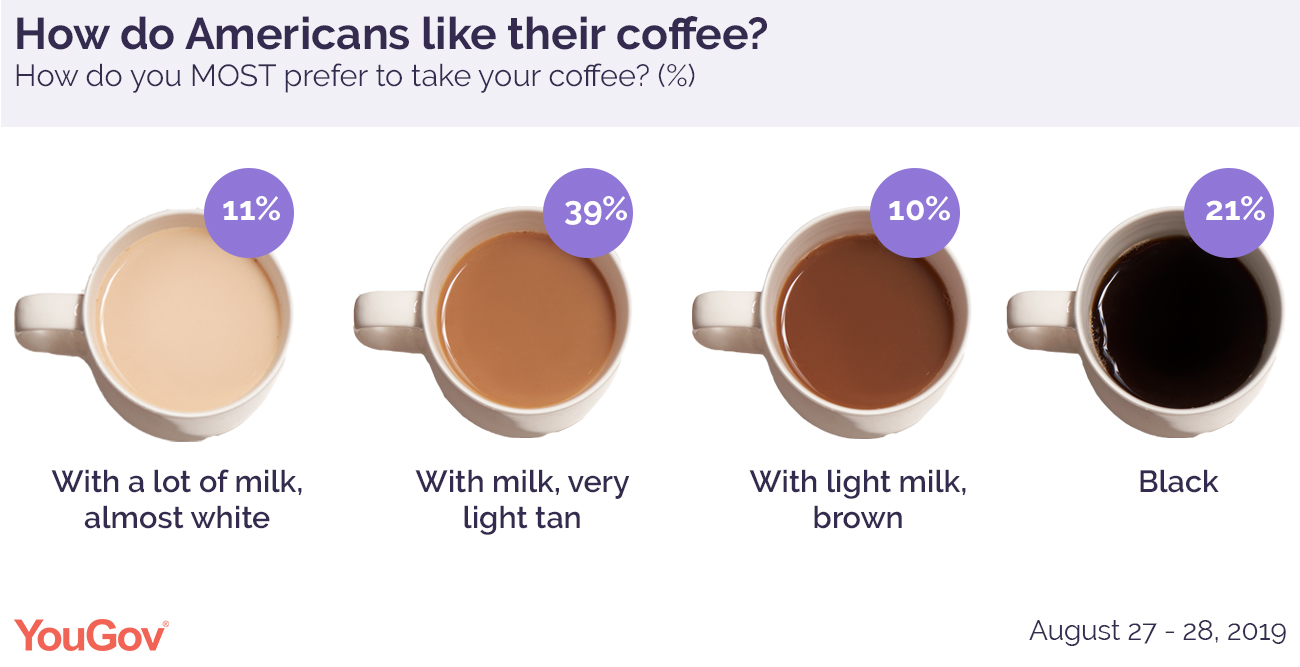

It seems that many Americans love to eat breakfast foods whether morning, noon or night. YouGov's latest data shows that how they eat breakfast foods varies. For starters how do they like their coffee:

- (81 percent) drink coffee

- (60 percent) add at least some milk to their coffee

- (39 percent) add milk until their coffee is light tan

- (11 percent) like it almost white with a lot of milk

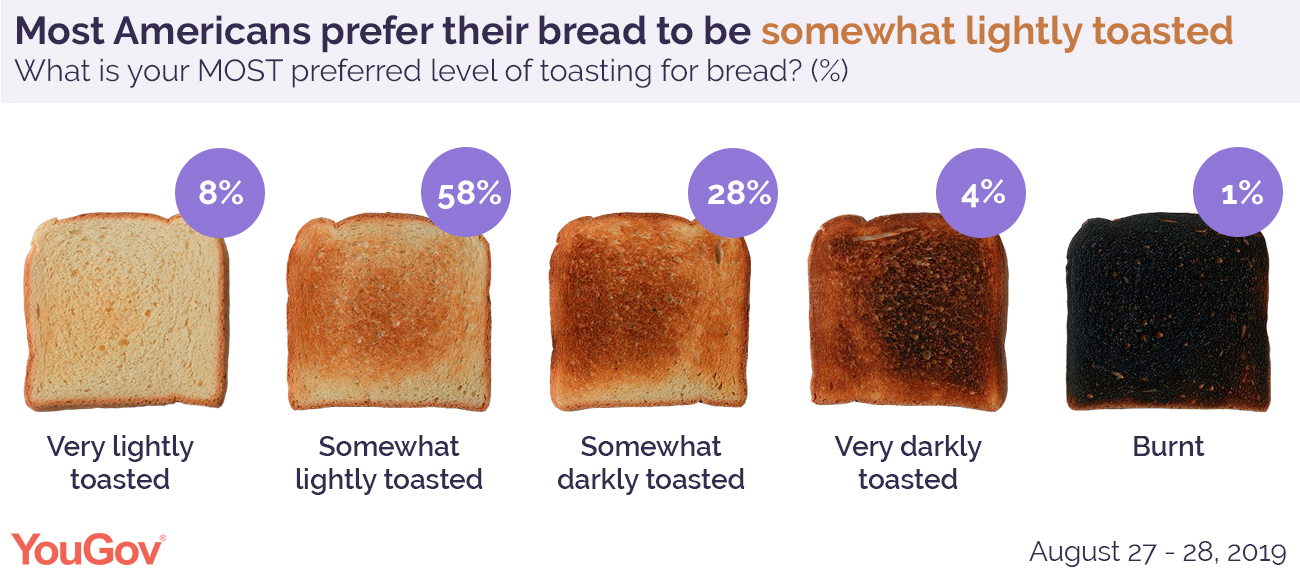

YouGov also surveyed Americans on how they prefer their toast, their eggs, and their bacon:

Toast

- (58 percent) prefer their bread to be “somewhat lightly toasted”

- (28 percent) prefer it to be a little bit darker

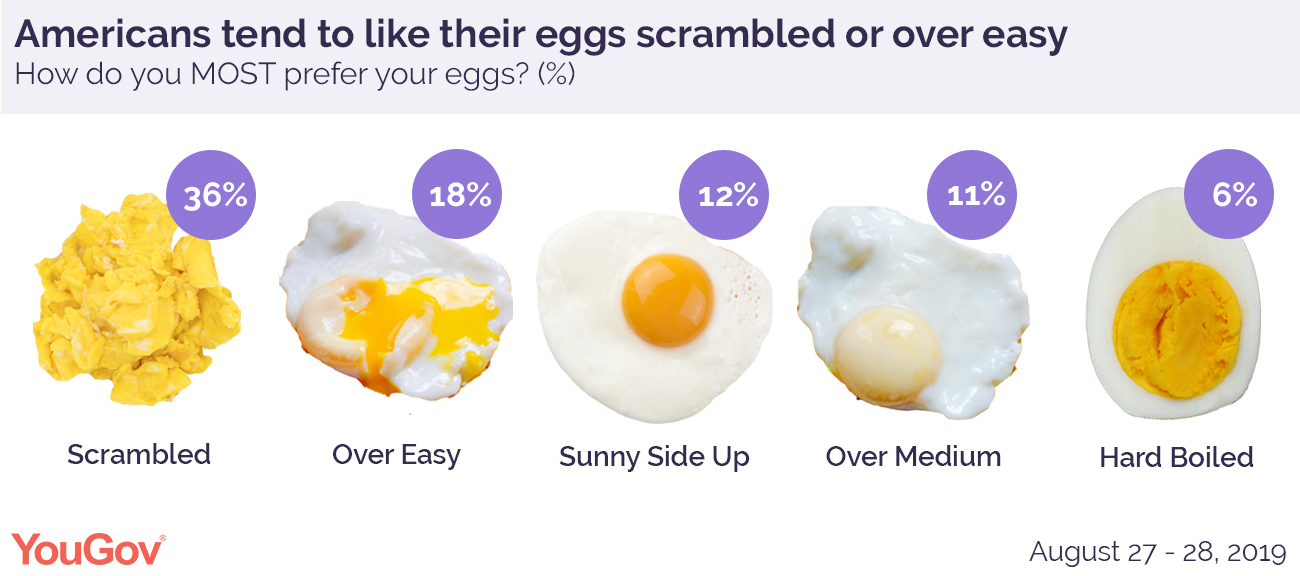

Eggs

- (36 percent) say scrambled is their preferred way to eat eggs

- (18 percent) eggs over easy

- (12 percent) sunny side up

- (11 percent) eggs over medium

- (6 percent) hard boiled

Bacon

- (93 percent) Americans, it’s not a real hearty breakfast without a few strips of bacon

- (37 percent) very crispy

- (34 percent) crispy

- (20 percent) very to somewhat chewy

Brits Love Chicken Shops

Well-heeled Brits are joining the nation’s chicken shop obsession, according to latest research from Mintel. Over the last year alone, the number of affluent Brits* visiting chicken outlets and restaurants has shot up from 40 percent in 2018 to 45 percent in 2019.

Meanwhile, those who have stable household finances are also now more likely to be enjoying the nation's chicken shops and restaurants. Almost half (47 percent) of those describing their financial situation as 'OK'** visited a chicken shop in 2019, compared to 41 percent a year earlier. This comes as the chicken segment has seen some worse-off consumers exiting the market. The number of Brits with a challenging financial situation*** visiting chicken shops dropped from 45 percent in 2018 to 42 percent in 2019.

The growing popularity of chicken shops/outlets among Britain’s better-off consumers comes at a time when 67 percent of consumers agree that burger and chicken restaurants are offering more healthy options than a year ago, rising to 72 percent of affluent Brits. Korean fried chicken is also proving particularly popular, with 71 percent of consumers saying they’re very/somewhat interested in this dish.

Following KFC's well reported supply chain issue in 2018, the value of the chicken restaurant market is expected to surge by 5 percent in 2019, with sales of just over £2.3 billion. Meanwhile, burger sales are faring well too. The burger sector is expected to grow by a meaty 4 percent in 2019, bringing sales to more than £5.2 billion. This year Brits are set to devour £7.5 billion worth of burgers and chicken across Britain’s restaurants and outlets.

Trish Caddy, Senior Foodservice Analyst at Mintel, said: “An improvement in the animal welfare of chickens is helping to attract a more affluent clientele to chicken restaurants and outlets, with chicken meals typically costing more than other fast food choices. More ‘exotic’ offerings, such as Korean fried chicken, are also broadening the appeal of chicken shops to these wealthier diners. The guilt-free indulgence of healthier, free-range chicken has clearly met affluent consumers’ value expectations, even if better chicken costs more than a burger. Well-off Brits' love for chicken also suits other food trends, such as eating more high-protein foods. This includes boneless chicken snacks such as bite-sized chicken fillets with dipping sauces, which are great for on-the-go consumption.”

It seems that fast food is picking up speed as consumers are increasingly enjoying this food via delivery services such as Deliveroo or Uber Eats. According to Mintel, almost four in ten (37 percent) consumers are ordering more food for home delivery from burger and chicken outlets/restaurants than they did a year ago. This compares to 25 percent who said the same in 2018. Eating in a relaxed and familiar surrounding is also likely to be driving demand, as 70 percent of takeaway and home delivery users say they prefer the comfort of eating at home than dressing up to go out.

“Consumers are increasingly expecting products and services to be brought directly to them. The burger and chicken market is making a serious effort to push into home delivery, with a trend of brands partnering up with delivery aggregators such as Deliveroo and Uber Eats. Eventually, big players may take back control of their delivery functions by managing an in-house ecommerce system, making it more accessible for them to expand at a faster rate than some of their appointed third-party delivery partners.” Trish adds.

Almost half (48 percent) of burger and chicken users would pay more to eat at a plastic-free burger/chicken outlet/restaurant, rising to 65 percent of 25-34 year olds. Interestingly, despite the media coverage and government-initiated campaigns in the UK to deal with plastic waste, there is still a lag in younger Britons’ awareness. Plastic pollution awareness is much higher in over-45s (62 percent) who are considerably more likely than 16-44 year olds (41 percent) to have heard news about single-use plastic.

Meanwhile, 44 percent of users would like burger and chicken outlets/restaurants to offer more dishes with meat alternatives/substitutes eg seitan and soy-based, with interest peaking amongst 25-34 year olds (60 percent). In reality, veganism (and even vegetarianism) is still very low down on British consumers’ dining out priorities, with only 9 percent citing vegan foods as something they would like to see more of when dining out.

“The tide is rising in favour of plastic-free, with diners even prepared to dip into their own pockets to ensure their environmental/sustainability values are achieved. Companies and local authorities will have to make recycling as easy as possible for consumers to have a significant impact on the environment.” Trish concludes.

* those who say “I have money left at the end of the month for a few luxuries or to add to my savings”

** those who say “I get by, but there's not a lot left by the time the basics are taken care of”

*** those who say “I'm making ends meet, but only just”

Growing Demand for Organic Food

According to Mintel Global New Products Database (GNPD), in the last 10 years, the total share of new global food and drink product launches with organic claims has risen from 6 percent to 10 percent between August 2009 and July 2019.

For younger generations, the social and environmental impact of consumption is of great importance and this is likely to help fuel future growth of the organic sector.

Mintel research finds that Europe is leading the way in terms of organic food and drink innovation, with almost a fifth of all food and drink products launched in Europe carrying an organic claim. In the 10 years to July 2019, the number of European food and drink launches with an organic claim has shot up from 9 percent to 17 percent, satisfying Europe's hunger for organics. Current leading innovators include France (accounting for 22 percent of all organic launches in Europe between August 2018 and July 2019), Germany (20 percent) and Spain (9 percent).

But it's not just Europe that is enjoying a greater variety of organic food and drinks; North America has also experienced an impressive increase in organic launches. The number of organic food and drink products has grown from 9 percent in 2009 to 15 percent in 2019 (Aug 2018-July 2019). While the availability of organic food and drink products in Asia Pacific, Latin America, the Middle East and Africa has risen slightly, less than one in twenty (4 percent) food and drink launches between August 2018 and July 2019 carried an organic claim in each of these regions. This is up from 3 percent in Asia Pacific and Latin America, and 2 percent in the Middle East and Africa ten years ago.

Speaking at Anuga, Katya Witham, Global Food & Drink Analyst at Mintel, says: “Organic produce has seen growing support among European consumers at a time of increasing concerns for wellbeing, health and the environment. Our research shows that the European market is spearheading organic food and drink innovation, with France, Germany and Spain leading the way. Although organic products have fully entered mainstream channels and continue to gain traction with shoppers, the organic segment still offers innovation opportunities across numerous food and drink categories. This is especially true in categories where organic claims have previously played a minor role, such as wine.”

Free-from and ethical messages gain importance in the European organic sector

Mintel research shows that the share of organic food and drink launches in Europe with “suitable-for” (free-from) claims experienced impressive growth over the past ten years, rising from 20 percent to 43 percent between August 2009 and July 2019. Ethical claims have also witnessed a similar increase during the same time period. While 23 percent of all organic food and drink launches in Europe were positioned as “ethical” and “environmental” ten years ago, this proportion grew to 41 percent in the year to July 2019.

“Organic claims are increasingly becoming part of wider health and ethical product positioning, hence the popularity of launches with free-from and ethical claims. Veganism/plant-based is one of the hottest trends in food and drink right now, so it seems natural that organic producers are linking the two. According to our research, almost half of vegan food and drink products launched in the past twelve months were positioned as organic. Given the trend towards veganism, plant-based organic brands are taking their lack of animal-derived ingredients to the next level, highlighting a more holistic approach.” Katya adds.

Millennials and Gen Z are the most likely to purchase organic food and drinks

Mintel research also finds that among consumers in France, Germany, Italy, Spain, and Poland, Millennials (aged 25-34) and Gen Zs (aged 16-24) are the most likely to purchase organic food and drink. Of these five countries, Italian Millennials are most likely (87 percent) to buy organic food and drink, followed by their German (86 percent), Spanish (85 percent) and French (81 percent) counterparts. In Poland, it’s Gen Z that is most interested in organic food and drinks, with 83 percent claiming to buy such products, compared to 80 percent of Polish Millennials.

What’s more, younger consumers are also more likely to pay higher prices for organic food and drink. This is especially true for Spanish Gen Zs: 38 percent say organic products present good value for money, in comparison to 26 percent of all Spaniards. Meanwhile, young Germans are less willing than their Spanish counterparts to pay extra for these products: 27 percent of 16-24-years-olds accept higher prices for organics, compared to 21 percent of the German population as a whole.

“Generation Z has grown up at a time when health and wellness is high profile. For younger generations, the social and environmental impact of consumption is of great importance and this is likely to help fuel future growth of the organic sector. Moreover, the prevalence of foodies among younger consumers creates an opening for more premium organic convenience products that are designed for the food-obsessed who want to eat well on-the-go or prepare upscale healthy food and drink easily and quickly at home.” Katya concludes.

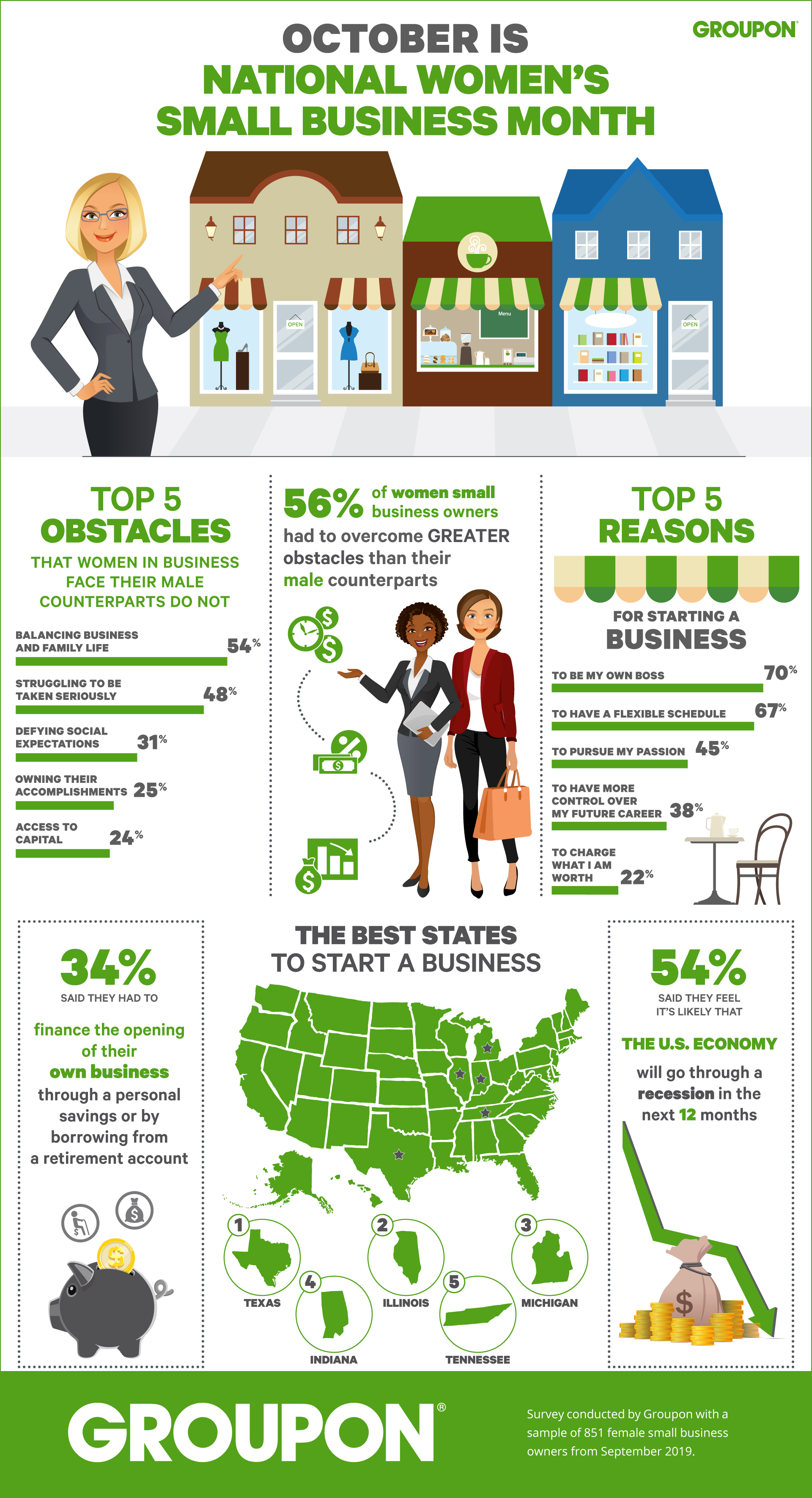

Obstacles for Women Small Business Owners

With one out of every five small businesses failing before the end of their first year*, opening and running your own business is an enormous challenge. According to a new Groupon survey, it’s even tougher for female entrepreneurs with more than half of respondents, 56 percent, saying that they had to overcome greater obstacles than their male counterparts and nearly 50 percent of respondents saying that they were held to a higher standard when trying to open their own business.

“As one of the largest marketplaces of small businesses anywhere in the world, we’re thrilled to honor female entrepreneurs and recognize the contributions and value they bring to our lives on a daily basis and to the communities we call home”

The poll, commissioned by Groupon for October’s National Women’s Small Business Month, surveyed more than 850 women small business owners to find out what sort of challenges they face, the best states for women to open their own business, why these entrepreneurs decided to become their own boss, how they achieved success and the most important issues they want to see addressed in the 2020 presidential election.

“As one of the largest marketplaces of small businesses anywhere in the world, we’re thrilled to honor female entrepreneurs and recognize the contributions and value they bring to our lives on a daily basis and to the communities we call home,” said Sarah Butterfass, chief product officer and Women at Groupon executive sponsor. “Many of the women that we interviewed had to overcome unique challenges in order to get their business off the ground and offered a number of key insights for other women thinking about starting their own business.”

Overcoming Unexpected Challenges

Seventy-one percent of women small business owners reported that they faced unexpected challenges when they opened their business. Some of these challenges included: balancing a business and a family, struggling to be taken seriously, defying social norms, owning their own accomplishments and gaining access to capital. Thirty-four percent of women small business owners said they had to finance the opening of their own business through personal savings or by borrowing from a retirement account.

Ranking the Best States to Start Your Own Business

Taking into account a number of different factors such as barriers to entry, economic conditions and available small business resources, Texas, Illinois, Michigan, Indiana and Tennessee ranked as the best states for women to start their own business. Massachusetts, New Jersey, Washington, South Carolina and Ohio rounded out the top 10. The top five ways identified by survey respondents in which state officials can help small businesses are: lowering or simplifying taxes, offering more small business resources, improving access to healthcare and insurance benefits, making housing more affordable and creating greater access to capital.

Becoming Your Own Boss

According to the survey results, being your own boss, having a flexible schedule, pursuing your passions, gaining more control over your future and receiving equitable pay were the top five biggest reasons women went into business for themselves.

Achieving Success

Of surveyed respondents, it took an average of nearly three years to make their small business a success. Entrepreneurs said that putting in the hard work, taking pride in the quality of their product or service, building a personal network, serving an underserved market or space and having innovative business ideas were the biggest keys to their success. Thirty-six percent of survey participants said they work more than 40 hours per week, and 76 percent stay up at night worrying about the success of their business.

Making Their Voices Heard in the 2020 Election

Women small business owners were split on the Trump administration’s impact on small business ––32 percent of those surveyed said that the administration has had a positive impact on their business and 31 percent said that it has had a negative impact. When it comes to the Democratic presidential candidates, more than half of the women small business owners who plan to vote during the primaries don’t think any of the candidates will positively impact small businesses. Of the respondents who expressed a preference, Sen. Elizabeth Warren was identified as the leading candidate who could have a positive impact on small businesses. The Massachusetts senator was followed by former Vice President Joe Biden, Sen. Bernie Sanders and Sen. Kamala Harris.

The top election issues identified by women small business owners were the following: healthcare, taxes, immigration, the economy and gun control. Finally, 54 percent of respondents said they feel it’s likely that the U.S. economy will go through a recession in the next 12 months.