MRM Research Roundup: Mid-February 2021 Edition

13 Min Read By MRM Staff

This edition of MRM Research Roundup features news of restaurant resiliency, dining trends in Canada, restaurant salaries across the U.S. and more.

Restaurant Resiliency

Throughout one of the most challenging years for U.S. restaurants, the industry demonstrated its resiliency against a variety of headwinds throughout 2020 by rising from a -35 percent traffic decline in April to a -11 percent visit decrease in December compared to year ago, reports The NPD Group. Although mandated dine-in restrictions have held back all restaurant segments, particularly full service, consumer demand for restaurant meals and the ability to serve the demand with a host of off-premises services, like digital ordering, delivery, drive-thru, and carry-out, are the silver linings that enable the industry to persevere.

Restaurant digital orders, which were growing prior to the pandemic, increased by +19 percent in January of last year to +145 percent in December compared to year ago, according to NPD’s daily tracking of consumers’ use restaurants and other foodservice outlets. Like digital ordering, carry-out, delivery, and drive-thru were also growing before the pandemic. Carry-out, which represents the largest share of off-premises modes, increased orders by +3 percent in January 2020 and by +10 percent in December versus year ago. Carry-out ended 2020 holding 46 percent of off-premises order share. Delivery, which was receiving a lot of attention before the pandemic even though carry-out and drive-thru have eight times more order volume, began 2020 with orders up by +1 percent and ended the year with a triple-digit gain of +137 percent in orders compared to year ago. Even with the triple-digit gain in orders, delivery still holds the smallest off-premises order share at 11 percent. Drive-thru, an ordering mode that was already well-developed at quick service restaurant chains when the pandemic hit, increased orders in 2020 from +4 percent in January to +22 percent in December versus year ago and ended the year with a 44 percent share of off-premises orders.

“Digital orders for pick-up and all off-premises modes will be a growth engine for the U.S. restaurant industry moving forward,” says David Portalatin, NPD food industry advisor and author of Eating Patterns in America. “Consumers, both new and former users, have now experienced the convenience of digital ordering, especially for carry-out and delivery, and will continue using these services long after the pandemic is over.”

What Feeds Us

Bluedot released the third installment of its State of What Feeds Us report. Over the course of the pandemic, the report has kept a pulse on shifting consumer behavior and its impact on restaurants. It offers insights into customer expectations to help restaurant brands navigate through what continues to be an uncertain consumer climate. The research, based on a survey of over 1,500 American consumers, was completed last month.

Highlights from the report reveal:

- Restaurant customers are showing clear signs of pandemic fatigue. Concern for safety protocols such as masks and gloves softened among consumers. They also expressed less anxiety connected to entering stores or restaurants. 69 percent were still experiencing some level of anxiety, a decline from 80 percent from last April.

- Consumers are becoming more impatient. Consumers favored shorter wait times over safety protocols.Their willingness to wait for restaurant orders dropped dramatically to an average of six minutes across drive-thru, curbside and in-store pickup options from 10 minutes just six months ago. Slow speed of service looks like a dealbreaker for consumers as 77 percent stated they will leave or consider leaving a restaurant if they see a long line.

- Curbside and in-store pickups are on the rise. 67 percent of consumers are picking up at curbside as often or more frequently now compared to 45 percent from last April. In-store pickups have also increased with 67 percent picking up in store as often or more frequently now compared to 55 percent last April. Of note, 53 percent of those who had not tried pickup last April have started to utilize the service.

- Restaurant drive-thru visits dipped slightly last month, but remain strikingly high. Consumer drive-thru visits dipped slightly from the last report with a decrease to 68 percent of those visiting as often or more frequently in January from 74 percent in August. However, the drive-thru still remains vastly more popular now than at the beginning of the pandemic with a 26 percent increase in consumers frequenting the drive-thru as regularly or more often since last April.

- Mobile real estate is competitive for restaurant apps. While the majority of consumers (85 percent) currently have at least one restaurant app on their phone, very few (17 percent) have more than five. However, 28 percent indicated they would be willing to have more than five restaurant apps on their phone. Brands that earn a spot will remain for at least six months according to 46 percent of consumers who stated they typically keep a restaurant app for at least six months.

- Consumers are downloading more restaurant apps and app usage has spiked. There continues to be a sharp uptick in mobile app usage since the start of the pandemic with consumers downloading and using restaurant mobile apps more now than ever before. The vast majority of consumers (82 percent) indicated that they have downloaded at least one new mobile app to purchase food or essentials.

- The data also revealed an increase of 134 percent among consumers who have downloaded three-to-five new apps and a 265 percent increase among those who have downloaded five or more new apps. The majority of consumers (68 percent) have one-to-five restaurant apps on their phone.

- Third-party delivery apps lag behind restaurant apps. 79 percent of consumers indicated they are ordering directly from restaurant apps more than once a month while 36 percent said they never order from third-party apps.

- Pandemic-era restaurant habits will outlast COVID-19. 8 in 10 consumers (78 percent) plan to continue their current dining habits even after the pandemic subsides.

“One of the big questions looming over restaurant brands during the course of the health crisis is whether the shift in consumer restaurant habits, including the growth of off-premise, will continue long term. It’s clear now from the data that while COVID-19 might have been the catalyst, the dramatic changes in consumer behavior are here to stay,” said Emil Davityan, Bluedot co-founder and CEO. “Restaurant customers are choosing a multi-channel approach to order pickup including the drive-thru, curbside, carryout and delivery. This means the operational logistics can no longer be a one size fits all approach and brands must meet consumer demand with a personalized, flexible solution that adapts to individual preferences.”

Other notable findings from the report include:

Mobile / Off-premises

The reasons consumers use mobile apps have shifted. Consumers were previously using mobile apps to limit contact, but they are now turning to mobile apps due to their ease of use. Ease of use increased 39 percent since last April while limiting contact decreased 14 percent. 86 percent have ordered directlyfrom a restaurant app in the last six months.

Fast food, fast casual and sit-down restaurant apps have seen the biggest jump since last April. Orders from fast food apps increased 38 percent, fast casual apps increased 71 percent, and sit down restaurants increased 88 percent.

Drive-thru

A whopping 91 percent visited the drive-thru in the last month.

Limited or no contact with staff still ranked as the top way consumers would feel safer though this number is down slightly from last April (40 percent in April compared to 35 percent now).

Curbside

The current curbside experience is failing. 55 percent expect to be automatically checked-in via the restaurant’s app and staff notified to bring items directly to their car, yet only 25 percent of respondents receive this level of service.

Personalization is key when it comes to curbside. 33 percent ranked being ignored upon arrival as one of their top curbside turn-offs.

Consumers feel safest when they don’t have to leave their car for curbside pickups.

In-store pickup

89 percent of consumers have utilized in-store pickups at restaurants in the last month. 53 percent of respondents who were not using in-store pickups at the start of the pandemic are now utilizing the service.

Safety priorities have shifted for consumers. In August, consumers would feel safest if staff was wearing protective gear and wiping down equipment. Now consumers want decreased wait times or no lines.

Wait time

Long wait times and lines are a deal breaker. 77 percent said that they would leave or consider leaving if they see a long line.Consumers now expect to wait no more than six minutes compared to August when a 10 minute wait time was acceptable.

At curbside, consumers ranked excessive waiting as their biggest dislike.

Safety

36 percent have turned to mobile or online ordering due to their fear of walking into a store or restaurant. Curbside pickups and the drive-thru have consistently ranked as the safest options amid COVID.

The third State of What Feeds Us report can be found here.

The Latest in On Premise

Nielsen CGA's latest COVID-19 On Premise Impact Report provides further insights into markets which are more ‘open’ than others, with the aim to assess what might happen as re-opening increases.

As the state which has been open the longest, we've focused this report on Floridians only. We have asked consumers key questions around their first visit and their general behavior ongoing.

Among the key findings:

- The most popular occasion for 'first visit' was with a partner / spouse. This could indicate that on first visits, people were more cautious, returning only with those from their household

- Currently, 63 percent of consumers are spending the same or more money (than pre COVID-19) on alcohol per visit – a promising note for the industry after a challenging period

- Different venues are providing category-specific opportunities on first visits back: beer dominates neighborhood bars and sports bars, while wine has a strong position in fine dining restaurants. Spirits do particularly well in neighborhood bars, and the top location for cocktails is in casual dining chains

QSR Hiring

According to Snagajob data, QSR positions were the most in-demand jobs across all applicable industries in January 2021, as the sector continues to rise despite the challenges of COVID-19.

In particular, these were the top positions sought by hiring companies:

- Team Member / Crew Member

- Barista

- Delivery Driver

- Cashier

- Shift Leader

Canadian Dining Trends

Although mandated dine-in restrictions throughout the pandemic netted a double-digit decline in visits to Canadian restaurants in 2020 compared to prior year, consumer demand for restaurant meals and the industry’s ability to serve the demand with a host of off-premise services, like digital ordering and delivery, helped to buoy the industry last year, reports The NPD Group. All off-premise order modes grew by varying degrees in 2020, while on-premise/dine-in orders declined by double-digits in 2020, according to NPD’s continuous tracking of Canada’s foodservice industry trends.

“The foodservice trends we saw as 2020 came to a close were established many months earlier,” said Vince Sgabellone, NPD foodservice industry analyst. “Pivotal among these trends is the continued importance of off-premise order modes. Canadians continued to support restaurants by dining-out at home. Off-premise orders represented about 80 percent of all restaurant visits by the end of last year.”

Key among the restaurant services consumers tapped into in 2020 was digital ordering. Foodservice digital orders, which were growing prior to the pandemic, experienced triple-digit growth in 2020 ending the year with a 142 percent increase in orders in December compared to year ago. The off-premise modes of carry-out and delivery recorded their fastest growth rates last year. Carry-out orders, which represents the largest share of off-premise orders, increased by +25 percent and delivery jumped by +98 percent in December compared to year ago. Drive-thru, an ordering mode that was already well-developed at quick service restaurant chains when the pandemic hit, increased orders by +45 percent in December versus year ago.

Total visits, physical and virtual, to Canadian restaurants and other foodservice outlets were down -16 percent in December versus year ago but quick service restaurants, whose business model has always been based on providing quick and portable meals, fared better with a -11 percent decline in visits. The full-service restaurant channel, most impacted by the dine-in restrictions, struggled to take advantage of the off-premise boom and realized a -37 percent loss in traffic in December compared to year ago, reports NPD.

“The Canadian restaurant industry is relieved to be putting 2020 in the rearview mirror, but it has experienced a decade of evolution condensed into several months,” says Sgabellone. “The pandemic has forced the evolution in ways that hadn’t been thought of before. Recovery won’t happen overnight, but the industry will recover with lessons learned and new ways of thinking already in place.”

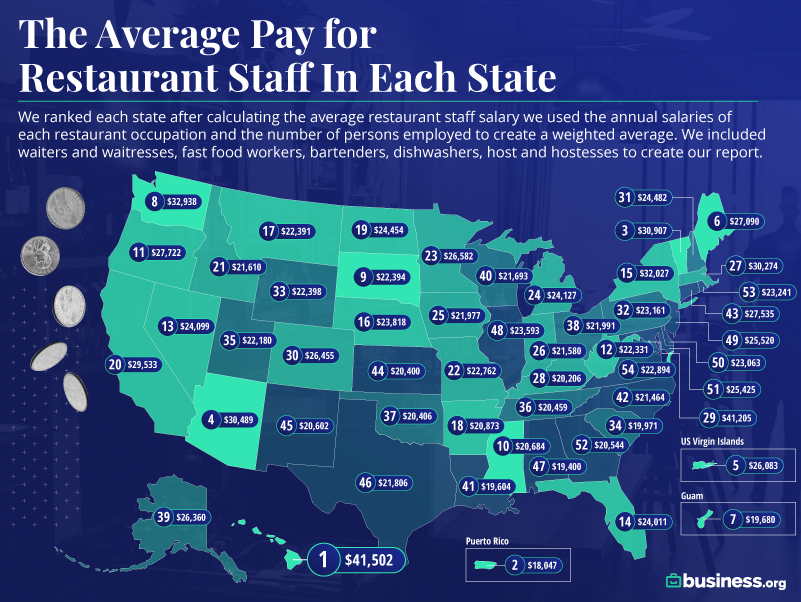

Restaurant Salaries

With over 8.1 million restaurant workers across the US and talks of raising the minimum wage, the team at Business.org wanted to know which states pay restaurant staff the most, top graph.

Nationally, restaurant workers earn an average salary of $24,861—that’s 54 percent less than all occupations across the country.

To see how more, click here.

Supporting Local

Based on responses from 1,000 U.S. adults, consumers are doing their part to support small businesses, with 53 percent buying from local restaurants and 33 percent shopping at local retailers – specifically to support them through the pandemic, according to a survey from Vericast's Valassis line. Additionally, consumers are more open to exploring new retailers and restaurants amid the pandemic. These behaviors have been driven by valuable offers (28 percent and 25 percent for retailers and restaurants, respectively), motivations to try something new (24 percent and 33 percent), and convenience/ease of ordering (19 percent and 25 percent).

Consumers continue to favor convenience and plan to maintain the accelerated use of pick-up and delivery services post-pandemic. New shopping behaviors adopted as part of their routine in the future, include the increased use of convenient services such as restaurant carry-out (29 percent), third-party delivery (27 percent), buy online, pick up in-store (BOPIS) (21 percent) and grocery delivery (17 percent).

“The extreme events of the past year led to dramatic shifts in consumer behavior,” said Carrie Parker, SVP of Marketing at Vericast. “People changed the way they live, shop and consume media, and our research shows that consumers are eager to discover new products and services and are desiring convenience and – above all – savings.

For marketers, this year it’s critical to really understand your target consumers’ shifting behaviors and motivations and evolve with them, engaging across new media and connecting dots to deliver meaningful experiences and offers that meet their needs in specific moments.”

Additional findings from the survey include:

Consumers miss in-store experiences

The elements consumers miss most about the in-store experience include browsing/discovering new products (45 percent), trying on apparel (40 percent) and testing products in-person (34 percent).

Streaming TV usage is accelerating

More than half (57 percent) of consumers have increased time spent watching streaming TV during the coronavirus pandemic.

Fitness resolutions begin at-home

While the first two months of each year are often a high-volume month for gym membership sales, only 13 percent of consumers plan to purchase in-person gym memberships; 12 percent plan to purchase virtual/at-home workout subscriptions.

The top planned purchases for consumers in the self-care and wellness categories over the next two months include stress relief products (23 percent) and exercise equipment (21 percent).

Super Bowl Pizza Stats

Although Super Bowl viewing parties looked different this year, sports fans’ undying love for a gameday feast and a piping hot slice of ‘za remain unmatched.

In its third year as the Official Pizza Sponsor of the NFL, Pizza Hut had its busiest day of the year. The proof is in the (millions of slices) pizza:

- 1.4+ million pizzas were sold on Super Bowl Sunday

- The most popular side sold on Super Bowl Sunday was wings

- More than 75 percent of one-topping pizzas sold during Super Bowl were pepperoni

- On average, guests in Kansas City spent 11 percent more per order than guests in Tampa Bay

QSR App Experience

Service Management Group (SMG) published new research that highlights how quick service restaurant (QSR) brands can drive app adoption. With digital usage on the rise across the restaurant industry, SMG conducted this study to understand what consumers want from branded QSR apps. SMG collected feedback from more than 16,000 consumers on QSR app usage. Here are three key themes from the research:

Consumers crave rewards – Eighty-three percent of respondents indicate they have at least one QSR app, and the top reason they cite for downloading the app is to earn loyalty rewards. Furthermore, when respondents were asked what they like most about their favorite app, the top response was the loyalty rewards program. While ease of use and speed in placing orders help drive app adoption, consumers expect to be rewarded for their brand loyalty.

Accuracy is the biggest barrier – While 91 percent of respondents indicate ordering via an app is about the same or a better experience than ordering in person, one in four consumers report they have experienced an issue with order accuracy when using a restaurant app. Though digital orders tend to include more customizations and create more complexity for staff, accuracy is simply one area where brands can’t afford to miss the mark.

App adoption requires a sound strategy – Among the 40 percent of respondents who have deleted an app in the past 30 days, 49 percent report they didn’t use the app enough and 33 percent cite difficulty placing orders or technical issues with the app. Furthermore, 40 percent of respondents who had difficulty placing an order indicate they are not very likely or not at all likely to place an app order ins the next 12 months. With more restaurant apps available than ever before, brands need to provide a seamless user experience and continually give consumers a reason to use their app.

“As digital usage continues to increase across the restaurant industry, brands need to strive to deliver a digital experience that’s on par with or better than the in-person ordering experience,” said SMG SVP of Research Paul Tiedt. “While ease of use and convenience are essential, what helps the top-performing branded apps stand apart is order accuracy and loyalty rewards.”

Gift Card Sales

Paytronix Systems, Inc., published the Paytronix Annual Restaurant Gift Card Sales Report: 2021, which finds that overall, 2020 card sales fell by 31.8 percent when compared to 2019 sales. With that in mind, quick-service restaurants (QSRs) came away the big winners by collecting a larger share of the market while full-service restaurants (FSRs) took the biggest hit. The holiday season remained a strong sales period for restaurants and accounted for more than 45 percent of all 2020 gift card sales.

COVID-19 upended the hospitality industry in March and continued to wreak havoc throughout the rest of the year. Fortunately, restaurants are among the most resilient businesses out there, and brands nationwide stepped up to the challenge, pivoting to online ordering, getting creative to keep guests safe on-premises, and redesigning their business models overnight to keep up with a rapidly evolving crisis.

“The executives in the restaurant industry are some of the most creative and innovative in the business world, so our bet is that we’ll see a great recovery as we head into 2021. We’re also seeing the demand for convenience increase, which will have an effect on e-gift, physical gift cards, and loyalty programs combined with stored value, as restaurants start to use all the levers of the single platform to drive visits,” said Michelle Tempesta, head of product and marketing for Paytronix.

The Paytronix Restaurant Gift Card Sales Report identifies several trends in closed-loop restaurant gift card sales and insights into the value of gift card programs in the industry during a turbulent, unprecedented year.

Quick-service restaurants fared well. QSRs, the service type that was best positioned to weather the pandemic due to its emphasis on takeout and drive-thrus, nearly matched its 2019 sales, realizing more than 96 percent of the number of cards sold in that year – a nearly negligible decline when compared to other restaurant segments.

In-store and third-party card sales were affected differently. In-store card sales fell less than 20 percent compared to 2019. Third-party sales declined most significantly: the number of cards sold through this channel fell 45.7 percent year over year. Cards sold through corporate channels fell 36.5 percent.

E-Gift card average load rose. In 2020, the average load amount on an e-gift card to a QSR was more than double the average load for a physical gift card.

May/June reflected the most depressed sales period. The number of gift cards sold during this period was significantly lower than in 2018 and 2019. The traditional Moms, Dads & Grads season presented a challenge for restaurants as many were just beginning to fully reopen for on-premises dining after state-mandated closures went into effect in March.

Card redemption was swifter. Gift cards were redeemed more quickly in the first 11 weeks after purchase as compared to 2018 and 2019. After the 11-week mark, cards sold in 2020 were less likely to be redeemed than those sold in 2019 or 2018.

“In-store sales realized the smallest decline in number of cards sold between 2019 and 2020, which we attribute to some brands running successful promotional offers, like 10 percent off or bonus card offers, that were not available at third-party retailers,” said Lee Barnes, Head of Data Insights, Paytronix.

To download the report, click here.