MRM Research Roundup: Mid-April 2020 Edition

13 Min Read By MRM Staff

This edition of Modern Restaurant Management (MRM) magazine's Research Roundup features the dismal March restaurant sales, security, loyalty, trends and teen consumer behaviors.

March Sales Decline

The rapid decline in sales during the second half of March due to COVID-19 was enough to push the industry down to its worst month in decades. Same-store sales for restaurants dropped by 28.3 percent in March. This update comes from Black Box Intelligence™ (formerly TDn2K™) data from over 50,000 restaurants and $75 billion in annual sales.

The 28.3 percent decline, as disappointing as it is, does not show the full impact the virus outbreak is having on restaurants. Same-store sales for the industry dropped by more than 65 percent during the last two weeks of the month.

“We have reported on restaurant sales and traffic since the last Great Recession, and this is something far beyond anything the industry has experienced,” said Victor Fernandez, vice president of insights and knowledge for Black Box Intelligence. “Although it is hard to classify anything as good news right now, there is a positive in the sense that the decline in sales may have reached bottom based on early April data. As more restaurants focus their undivided attention on their off-premise offerings and guests adapt their consumption to this new environment, plus some of the government relief measures take effect, some small improvements may lie ahead.”

Guest Counts Plummet as their Guests Shelter in Place

Same-store traffic fell by 29.2 percent during March. As with sales, it was not until the last 2 weeks of the month that traffic was severely impacted by the measures imposed to try to slow down the COVID-19 spread. As normal routines for work, school and other activities were disrupted by people sheltering at home, restaurant guest counts fell close to 70 percent in comparable stores during the end of March.

Guest Check Growth Flat, Widening Spread Between Segments

Average guest checks grew by about 2.4 percent year over year in March. But as much of the story written during the month, it is really the last two weeks that require special attention. By the end of the month, guest check growth became essentially flat year over year.

The real story there was the widening check growth dynamics between segments. Limited-service restaurants (those in quick service and fast casual) had a sharp acceleration in their guest check growth, as consumers likely shifted to larger off-premise orders to feed multiple people at home. Meanwhile, guest checks dropped considerably for full-service restaurants, a drop that was fueled in large part by beverage sales being almost completely eliminated by the shift to off-premise only operations. Alcoholic beverages, in particular, can have an enormous impact on guest checks, especially for bar and grill and more upscale restaurants.

Full-Service Restaurants Hit Hardest by the Crisis

Fine dining and upscale casual were the worst performing segments during March based on same-store sales growth. Family dining was another segment that was hit hard, which includes many buffet-based concepts.

With restaurant operations shifting to off-premise sales only, concepts that were developed with off-premise as an essential part of their business are naturally faring much better. Quick service and fast casual were the best performing segments based on sales growth during March. While full-service restaurants were experiencing same-store declines of more than 70 percent year over year by the last week of the month, fast casual’s decline was about 50 percent and quick service lost only about 30 percent of its sales during the week.

All Day Parts Suffering

The sharp decline in sales has reached all restaurant dayparts as regular daily routines got upended by the social distancing guidelines. As the pandemic effects started to hit the entire country late in March it seemed, initially, that breakfast and mid-afternoon sales were holding up better than the rest. However, by the last week of the month breakfast sales growth fell in line with the declines being reported for the lunch and dinner day parts.

Mid-afternoon sales remain as the best performing day part based on same-store sales growth by the end of the month, while late-night sales have been the most negatively affected since early in the crisis.

Regions with Large Outbreaks See Most Negative Impact

By the last week of the month, the regions experiencing the worst declines in restaurant sales were those where the biggest COVID-19 outbreaks have occurred, as well as regions with large metropolitan areas of high population density. Same-store sales dropped by more than 70 percent for New England, the Western region, New York-New Jersey, the Mid-Atlantic and California during the last week of March.

However, performance was not much better for the rest of the country during the final week of the month. In fact, the Southeast was the only region that experienced less than 60 percent decline in restaurant sales year over year.

For projections, click here.

Engaging Customers During COVID-19

A MomentFeed survey found that, despite high levels of concern and changes in daily routines, local restaurants and stores can still earn consumer trust and business during COVID-19. In fact, 86 percent of consumers indicated that local restaurants and stores could proactively earn their business, even in the current climate. Here are eight ways to tackle this opportunity.

Free delivery – Free delivery was cited by nearly half of all survey respondents as something stores and restaurants can do to earn their business during COVID-19. This indicates that free delivery is quickly becoming an expectation or at least a defining reason for choosing one brand over another. Aggregator services like GrubHub, Instacart, and UberEats have gladly stepped in to help, and restaurants with an infrastructure to do so, have followed suit.

Take-out options – For restaurants unable to ramp up a delivery service or worried about the commission cut of food aggregators, takeout being the second best way to earn business is encouraging. Consumers are still very willing to get mobile and visit your stores for pick-up. However, they need to know that you have this capability.

Easy online ordering – Easy online ordering was nearly tied for second. Consumers prefer an easy experience when they do choose to order food or buy products or services online.

Curb-side pickup – As consumers look to limit exposure to other people, curb-side pickup is another service that seems to be gaining popularity, coming in at number four. Things to think about here are whether you are providing a COVID-sensitive pickup experience. How are you facilitating parking and making it easy for a customer to pick-up their orders with no/low interactions with others? Are all of your staff clearly wearing appropriate face masks and gloves to ensure minimal risk of transmission to your customers?

Transparency into work environment precautions – Many restaurants and stores are publishing the precautions they are taking to ensure the safety of customers and employees. According to our survey, consumers reference these precautions before making a purchase decision.

Fast delivery – While not as highly valued as free delivery or easy online ordering, fast delivery is still appreciated.

Discounts and offers – Consumers are clearly looking to economize at a time when home finances are under pressure and uncertain. So it is quite unsurprising that over a third of respondents indicated discounts and special offers as a way to earn their business, it may be something to test. Consider a gift card with purchase to earn repeat business or a free with purchase high-margin item with perceived value (coffee / soda / etc.).

Commitment to local jobs – While commitment to local jobs was lower on the list of ways restaurants and stores can earn consumer business, it is still encouraging to see consumers taking notice. Doing good at a time like this is a rare opportunity and a chance for brands to build respect in their communities that may not pay off immediately, but will hopefully boost their brand and sales in the long run.

Food and Alcohol Sales Trends

New Nielsen CGA data, acquired by surveying U.S. consumers (March 28-29) and tracking food and alcohol sales trends (two weeks ending March 21 and March 28) within the U.S. on-premise space.

Overwhelmingly, the main focus was on take-out/delivery, both from a food and alcohol point of view. Here are highlights:

- Take-out is key to sales for outlets that are still operational, growing by +110 percent for the week ending March 28 vs. an average week.

- Two-thirds (66 percent) of consumers say they have ordered take-out/delivery in the past 2 weeks.

- Of those ordering take out/delivery, more than one-third have been ordering food from venues they have eaten or drank in before.

- 15 percent are ordering take out/delivery with alcoholic drinks

- This behavior is more popular with younger consumers; one in four 21-34 year olds have ordered alcoholic drinks with take out.

- The top factor influencing the choice to buy alcoholic drinks with take out/delivery relates to ease and safety. 58 percent did so to avoid a trip to get food and drink at the grocery store/supermarket or liquor store.

Gift Card Sales Boom

According to BentoBox, At the beginning of March, there was a gift card sales increase by 977 percent, with Americans spending over $100,000 per day to support their local restaurants at peak

Since then, gift card sales have declined, but online ordering and merchandise sales have both increased steadily:

Online orders have increased 50 percent week-over-week for the last three weeks

Merchandise orders–t-shirts, home-cooking kits, or anything else off-menu–have also steadily increased between 30-50 percent week-over-week for the last three weeks

For more data, click here.

Latest Sense360 Data

Here are some new findings from Sense360's daily research on COVID-19,

Sentiment & Employment Status Updates:

Close to 17 percent of people are income insecure at this point, indicating how important value is to consumers.

The percent of people who think COVID-19 is a bigger threat than most realize has continued to grow, with more than 2/5 of people believing that

Consumers increasingly believe that Coronavirus-related restrictions will carry into the summer

Over seven percent of consumers asked, say that they are on temporary, unpaid leave/furloughed

Transaction Data Deep Dive:

Dollar is up in terms of transactions as well as basket size

There appears to be a slowing in basket size growth in retail channels; momentum peaked in the first couple weeks of the pandemic

Shoppers likely stocked up on lower-frequency categories early on and now we're seeing some of the smaller fill-in trips to continue to sustain our households in-between larger tripsAmazon is up, though not as much as Dollar, in terms of spend/capita and appears to be gaining momentum in recent weeks.

Foot Traffic Decline

Zenreach monitors Walk-Through™ data in thousands of businesses across the North America. In a newly released deck, it shows the steep decline of foot traffic to America’s businesses in March 2020 due to the spread of Covid19 and associated governmental “shelter in place” orders.

-

San Francisco was among the first cities to see a decline in foot traffic, dipping during the first two weeks of the month and 61 percent YOY.

-

New York businesses saw a decline beginning as early as March 9, 2020 and now show a 63 percent YOY decline.

-

Phoenix and Chicago are among the cities that experienced no dropoff until the weekend of March 14-16, 2020. Zenreach experts expect more material declines are yet to come for these markets.

-

In New Orleans, revelers held on through Mardi Gras, dropping off much later and more rapidly. Traffic is now down 71 percent but was otherwise increasing until mid-March.

-

Despite reports otherwise, Boston showed a decline YOY during St. Patrick’s Day weekend.

-

While food and beverage had been declining steadily, retail is generally trending up. This data accounts for supermarkets and some shopping centers.

First-Time Delivery Is Up

According to Valassis, increasing demands for delivery: 12 percent of consumers have used restaurant delivery services for the first time, while 20 percent have increased the frequency in which they are using these services in response to the ongoing pandemic.

Customers act on impulse decisions: For third-party delivery services, the path to purchase is often very short – 77 percent of consumers are making their restaurant decision less than 30 minutes before they order.

Valuable deals can motivate customers to try something new: 63 percent of customers have changed their mind about what restaurant to order from because of a coupon or promotion presented to them while browsing.

New F&B Trends

New research from Social Standards says in the past two weeks, we’ve seen previously trendy diets and environmentalism/sustainability take a backseat, as consumers turn their attention towards finding ways to support their immune system, help local businesses, and relieve their stress.

Overall, it is an increasing possibility that social distancing may continue through the early part of the summer. While bev-al products that tend to receive a seasonal summer boost stand to lose in their traditional channels (i.e., restaurants, bars, clubs, etc.), they may benefit elsewhere as we see shifts in how consumers engage with alcohol amidst social distancing. For example, wines, whiskey, and classic cocktails are now being consumed during virtual happy hours instead of bars and restaurants and may stand to benefit from these new consumption behaviors. Rose and hard seltzers may be negatively impacted by consumers not being able to go to beaches, pools, and summer parties. Still, some of this expected downturn may be salvaged by people who are now consuming them during Netflix home viewing. Finally, whiskey, wine, and homemade cocktails have strong associations with at-home consumption and thus may not lose out as things shift away from bars, clubs, and other nightlife establishments.

Same-Store Sales at McDonald's

McDonald’s said its global same-store sales fell 22 percent in March as the coronavirus pandemic led the fast-food chain to close its dining rooms.

Placer.ai created a report in mid-March that shows McDonald’s foot traffic in light of QSR/fast food resiliency amidst COVID-19.

As an example, on April 3rd the percent of change in Foot Traffic was down 62 percent YoY.

Emotional Connection and Loyalty

Studying more than 5,000 customers in a loyalty/rewards program, researchers at Washington University in St. Louis found both a financial and emotional connection to businesses offering such contact, if not deals.

“It is often easier for companies to get in touch with their loyalty program members than with other clients,” said Yulia Nevskaya of the Olin Business School. “The right tone and message and being sensitive to likely shifting needs of consumers during and after the COVID-19 epidemic should definitely help.”

Read more here.

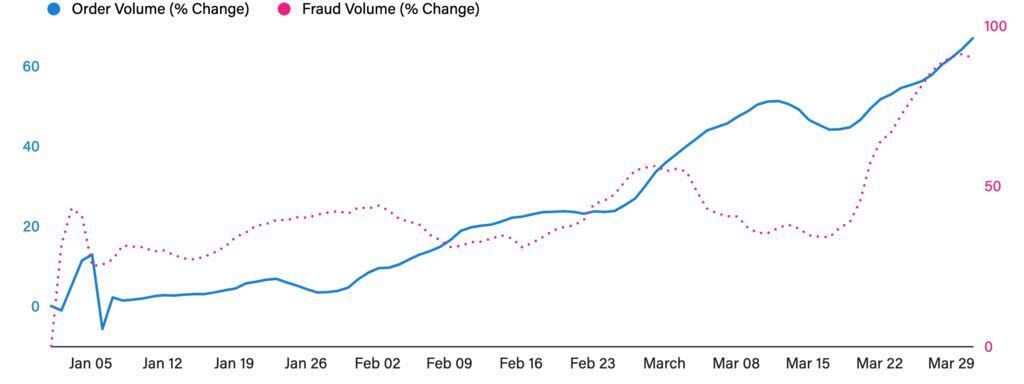

Payment Fraud Up

COVID-19 has rocked the food and beverage industry – but perhaps not in the ways you may think. With social distancing at play, consumers have increased their use of mobile payments, food and grocery delivery, and BOPIS (buy online, pickup in-store). New data from Sift shows that this industry has experienced a 27.3 percent sales increase between March 1-23.

While sales may be booming, so too is payment fraud. Sift’s data shows a clear correlation that as sales have peaked, so have fraudulent purchase attempts – indicating that fraudsters are taking advantage of the increased volume in activity in the hopes of flying under the radar. From January 1 – March 31, order volume was up 60 percent and fraud volume was up 90 percent.

Hand Washing Survey

If there is some good news in the age of coronavirus, research from the Healthy Hand Washing Survey shows that during the past 11 years an increasing number of Americans are heeding the message about washing their hands to protect themselves from flu outbreaks. The question then becomes: Are facilities equipped to support hand washing as people return to their regular public activities?

In 2009, the year H1N1 hit the United States, only 45 percent of Americans said they washed their hands more frequently or thoroughly in response to flu virus outbreaks. By 2019, the number of flu-fighting hand washers in the U.S. had risen to 79 percent.

A national focus on outbreaks does have an affect on hand hygiene. 50 percent of Americans say news coverage of cold and flu outbreaks has a "very large" or "somewhat large" impact on their hand washing behavior. Women and their hand washing habits are more likely to be impacted by news coverage than men (53 percent vs. 47 percent).

“The steady rise in hand washing diligence in America may, in part, stem from several stand-out flu seasons over the past decade – particularly flu outbreaks in 2009, 2015 and 2018,” says Jon Dommisse, director of strategy and corporate development for Bradley Corp. “Now, the unprecedented spread of coronavirus has placed an even more intense spotlight on the critical nature of thorough hand washing with soap and water for at least 20 seconds.

“Hand washing in public facilities will be exceedingly important in the coming weeks and months as people return to workplaces, offices, schools, restaurants, stores and other gathering places,” Dommisse said. “It’s essential we take advantage of every opportunity to wash our hands whether we are at home or in public.”

According to 11 years of Healthy Hand Washing Survey findings, the following actions encourage hand washing in public restrooms:

Hand washing signage. Almost 40 percent of Americans say they’re more likely to wash their hands after seeing a sign that requires employees to wash before returning to work.

Clean and stocked restrooms. The top two reasons Americans don’t wash their hands after using a public restroom are lack of soap or paper towels (34 percent) and restroom sinks that are dirty or not working (21 percent). In addition, 85 percent of Americans say they hurry to get out of a restroom if the conditions are unpleasant.

Touchless hand washing fixtures. While keeping them cleaner and better stocked is Americans’ most desired improvement in restrooms, making everything touchless is next on their wish list. People go out of their way to avoid contact with germs in restrooms. 65 percent use a paper towel to eliminate hand contact with doors and faucets and 44 percent of people operate toilet flushers with their foot.

Taking Stock with Teens

Piper Sandler Companies completed its 39th semi-annual Taking Stock With Teens® survey, which highlights discretionary spending trends and brand preferences from 5,200 teens across 41 U.S. states with an average age of 16.2 years. Generation Z, which contributes approximately $830 billion to U.S. retail sales annually*, represents an influential consumer group where wallet size and allocation provide a proxy for category interest.

This year’s Spring 2020 survey was impacted by the COVID-19 pandemic. The survey was conducted from February 17 to March 27 with several teens taking it while quarantined at home – most notably during the last three weeks of the survey. Students answered the survey at home as part of an online learning module Piper Sandler incorporated with partner, DECA. Finally, we received lower responses from the Northeast – the part of the U.S. which has suffered the most from COVID-19.

“Our Spring Teen Survey was conducted during a time of significant upheaval as the world (and U.S. teens) grappled with the realities of COVID-19. In fact, we believe the majority of our responses came from teens taking the survey from their own homes. Not only was ‘Coronavirus’ listed as the No. 2 social/political concern among teens, but we saw a significant uptick of teens worried about the economy along with a corresponding 13 percent drop in ‘self-reported’ spending versus just last year,” said Erinn Murphy, Piper Sandler senior research analyst.

“Today’s teens are more connected than ever before—they spend an average of 12 hours on social media per week, 53 percent name Amazon as their top e-commerce site, Netflix is their go-to choice for daily content & 85 percent own an iPhone. As it relates to brand preferences, we continue to see casualization of fashion march higher—Nike gained share as the No. 1 brand & lululemon hit a new survey high as the No. 6 preferred brand.”

Spring 2020 Key Findings

Spending & Shopping Behavior

Food continues to be teens’ No. 1 spending category at 25 percent of wallet share, up from 23 percent in Fall 2019

Amazon continues to climb as teens’ No. 1 preferred online shopping mindshare at 53 percent —10x higher than the No. 2 ranking, Nike

Cosmetics spending for females hits 10-year low with spending down 26 percent Y/Y to $103/year

78 percent of female teens use online influencers as a source of discovery for beauty brands and trends

Teens indicated they spend an average of $89/year on handbags — a new survey low and compares to peak spending of $197/year (Spring 2006)

Average video game spend by teens over the past 15 surveys is $197

Brand Preferences

Chick-fil-A remains No. 1 restaurant for 5 surveys; Starbucks retains double-digit share

Kellogg most preferred snack brand among teens

Ulta maintains No. 1 preferred beauty destination against Sephora for third survey in a row

Netflix surpasses YouTube as No. 1 daily video consumption; Disney+ debuts in top 5 ahead of Amazon and Apple TV+

85 percent of teens own an iPhone and 88 percent expect an iPhone to be their next phone, both new all-time survey highs

The Piper Sandler Taking Stock With Teens® survey is a semi-annual research project that gathers input from 5,200 teens with an average age of 16.2 years. Discretionary spending patterns, fashion trends, technology, and brand and media preferences are assessed through surveying a geographically diverse subset of high schools across the U.S. Since the project began in 2001, Piper Sandler has surveyed more than 185,000 teens and collected over 46.2 million data points on teen spending.