How to Analyze Restaurant Financial Statements and Identify Growth Opportunities

5 Min Read By Ryan Grundy

Restaurant financial statements are an untapped source of potential growth. After all, they are made up of data, and you can use data to drive improvement.

How do you determine which data to look for to optimize your statements?

How to Analyze Different Restaurant Financial Statements

To help you make the most of your restaurant financial statements, let’s break down how you should approach a few different types.

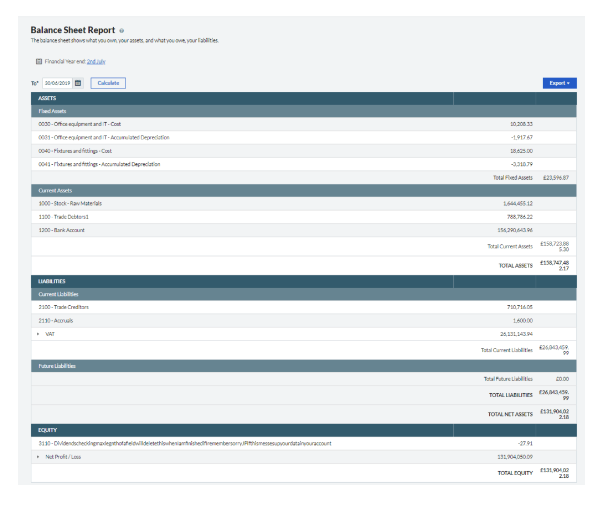

Balance Sheet

This document provides insight into the current state of your finances (up to a specific date).

Here’s what you can do with a balance sheet.

Identify revenue and expenses

What are you spending money on, and where are you earning the most? It’s always worth knowing your bestsellers and your biggest financial drains.

By identifying which dishes are your most profitable, you can start to make informed decisions. For example, you might use your best-seller to lead your next marketing campaign or decide to replace a dish that isn't providing enough return.

Compare current financial data to the previous fiscal quarter/year

It’s important to know how your current performance stacks up against your past progress.

If you’re doing worse than before, use your balance sheets to try and determine when this change happened; if you’re doing better, identify the factors behind your newfound success so you can capitalize on these.

Identify pain points and strategize on how to resolve them

There are many challenges and opportunities for those in the restaurant sector, but not all of these affect every business in the same way. The more you know about the pain points you’re struggling with—financial or otherwise—the more easily you can fix them.

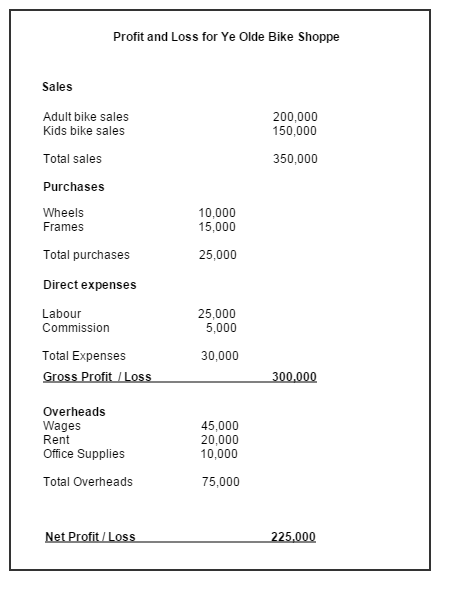

Income statement (P/L statement)

This document shows restaurant owners how much they’ve made versus their losses, so they can determine whether their ROI was sufficient to balance their spending.

Here are some other useful things you can do with a P/L statement.

Analyze sources of income

Where does your revenue come from, and how varied are these sources? Can you build on a single source, and if so, how can you do this?

These questions should guide your income analysis and be used to shape your attempts at increasing growth.

Keep in mind the effects of the season on sales

Restaurants have to be mindful of seasonal variations in customer spending. For example, the Christmas period typically brings with it increased sales, whereas January signifies a downturn in disposable income for most consumers.

Understanding your high and low seasons will help you plan more effectively for the year. You’ll know when to recruit more staff to deal with demand and when to hold off on ordering more stock. It will help you manage your finances more efficiently and put you in a better position to ride out those quieter months.

Review the cost of goods sold

Are your prices appropriate for your goods, and will they need to be adjusted in the future? You’ve got to make sure your prices reflect factors like inflation, the cost of ingredients, and customer expectations.

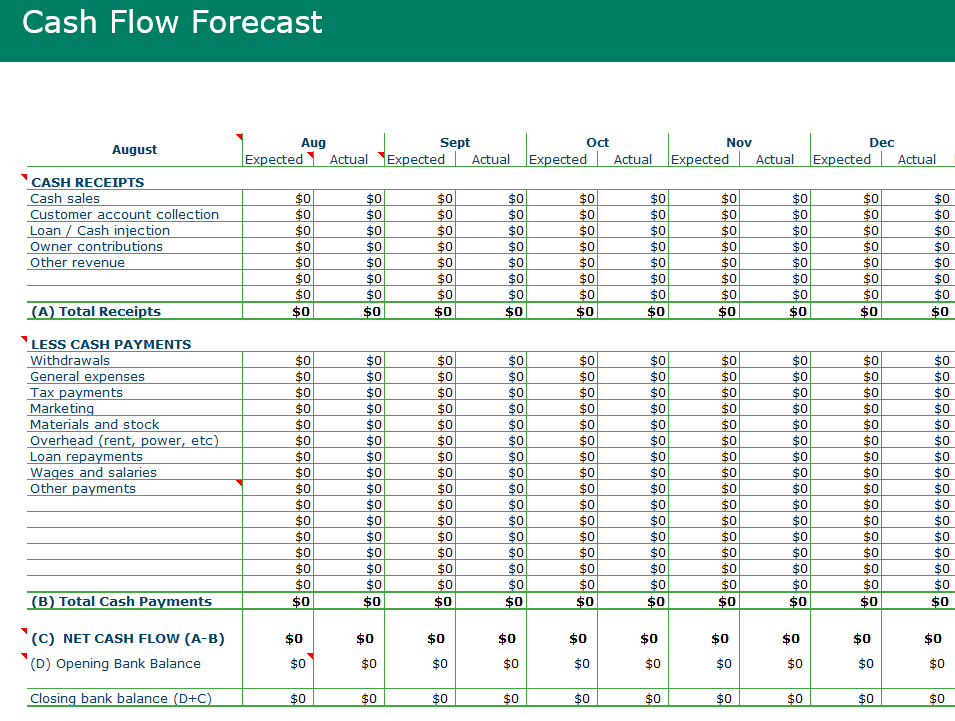

Cash Flow Statement

The term cash flow describes the money moving into and out of your business. A cash flow statement details what this flow looks like for your restaurant.

You can use it for the following purposes.

Compare the difference between cash income and cash expenses

Are you spending more than you’re earning, or do your earnings justify the expenses that come with them?

A cash flow statement makes it simple to see how your income and expenses compare. This makes it easier to determine whether new sources of income are generating enough ROI to continue being a valid option.

Identify expenses, including debts, and strategize how to address them

It’s no secret that certain uncontrollable factors, such as inflation, affect restaurants. Ingredients become more expensive, and consumers tend to cut spending on leisure activities, choosing to eat out less. But that doesn’t mean you can’t lessen your expenses to compensate.

If you have a clear breakdown of where your money is going, you’ll have an easier time eliminating unnecessary sources of expenditure. This reduces your outlay and prepares you to start saving and paying off debts.

How Restaurants Can Create Better Financial Statements

If you’re planning to use financial statements to find ways to grow your restaurant business, you’ll need to optimize how you create them.

So, where should you start? The following tips will guide you through the process of creating the best possible statements for your restaurant.

Keep an updated and organized record of financial data

It’s a huge waste of time to comb through disorganized information whenever you want to draw up a financial statement. To avoid this, make sure you’re keeping your data well-organized and updating it regularly.

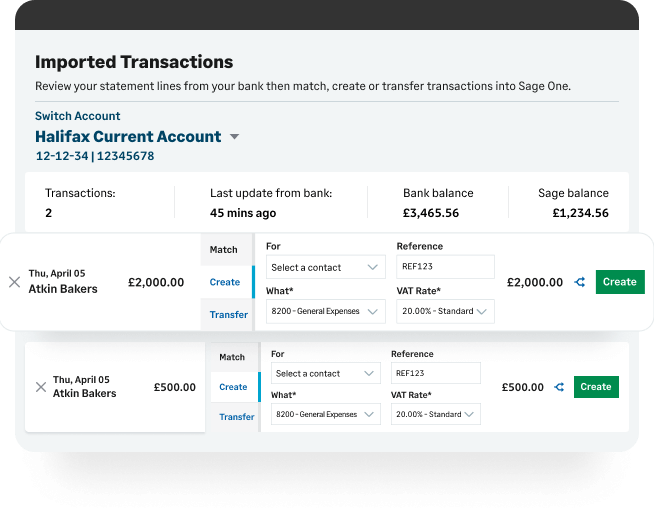

Dedicated restaurant accounting software does this automatically. All you have to do is enter your current data, and you’ll then be able to store new information in one convenient, easily accessible, and unified location. This comes in handy if you’re running a single restaurant in the UK or several across different states in the US.

Take advantage of financial technology and automation

The modern business world is saturated with useful tech that will help you get things done more effectively and in less time. Restaurant financial statements are no exception.

You can also use automation to complete repetitive tasks, such as verifying and validating financial information.

Always have a forecasted financial statement ready for comparison

It’s a good idea to take a look back at your financial predictions to see how accurate they were.

This ensures that predictions become steadily more accurate over time and that you’re well-prepared for anything that comes your way.

This is another instance where a specialized tool can be immensely helpful. For example, forecasting tools can use your data to generate predictions.

Identify pain points that affect restaurant revenue and expenses

You can’t always predict which future events will impact your revenue and expenses. That said, you can eliminate recurring problems by spotting and then resolving pain points.

To do this, you’ll need to follow a similar procedure to the one we described for identifying growth opportunities—only instead of looking for potential, you’re looking for problems that keep cropping up.

Plan restaurant strategies according to data and trends

Data is always important, and what’s also essential is looking at emerging patterns in your industry and in consumer behavior. If everyone else is going cashless, for example, you don’t want to be the only restaurant still asking customers to pay with notes and coins.

Your restaurant financial statements are immensely useful, for staying on top of your finances and continuing to grow as a business.

The better their overall quality, the more easily you’ll be able to pinpoint ways to build and scale your venture.