According to a Recent Study/Survey … Mid-April 2017 Edition

35 Min Read By MRM Staff

Just how many restaurants are there in the U.S.?

How do most people say caramel?

Do coupons drive restaurant traffic?

Which dish do people prefer on a first date?

Read on to learn the answers to these questions and more as Modern Restaurant Management (MRM) magazine’s popular research wrap-up returns for mid-April.

Restaurant Numbers Growing

CHD Expert released its 2017 Restaurant Unit Report detailing the Full Service Restaurant (FSR) and Limited Service Restaurant (LSR) landscapes in each of the 50 United States and Washington, D.C. broken down by menu type and segment. The report further segments chain and independent operators.

Vermont has the largest percentage of independents, while Kentucky has the largest percentage of total FSR chain restaurants.

As of March 2017, CHD Expert reports that there are more than 700,700 restaurants in operation across the United States, showing a three percent positive net growth of almost 22,000 restaurant locations since March 2016.

As the U.S. restaurant landscape continues to rebound, the independent restaurant landscape saw a five percent uptick, resulting in a positive net change of more than 24,000 units compared to 2016. CHD Expert defines an independent as a restaurant with less than 10 units in operation, whereas a chain has 10 or more.

In total, 37 states in the union saw positive growth since 2016, as did D.C., where our nation’s capital grew by 2.7 percent. Growth on the state level was most remarkable in New York, Texas, Illinois, North Dakota and Michigan.

Eleven states had a decrease in total restaurants in operation since 2016, lead by struggling West Virginia, which shrank by 2 percent. Alaska and Maine were the only other states to see a net loss of > one percent of their total restaurants. Given all of the turnover and new openings that has occurred over the past year, Delaware and Oregon had flat growth (less than .01 percent variance).

Considering growth by Menu Type, the strongest uptick was among Bar & Grills. This menu type added more than 4,400 units nation wide, as was the only menu type to have a net increase in every state (and D.C.). The Latin American and Bakery/Donut Menu Types also saw strong growth nation wide. The Chinese Menu Type saw the largest decrease.

Within the 2017 FSR landscape, Vermont has the largest percentage of independents, with 98 percent of the state’s FSRs being classified as independent. With regard to chains, Kentucky has the largest percentage of total FSR chain restaurants, at 17 percent of the state’s FSR landscape.

On the 2017 LSR front, Iowa is the state with the largest percentage of chain restaurants within its borders, with chain restaurants making up 74 percent of the state’s LSR landscape. New York is on the opposite side of the spectrum and a state where independent LSRs prosper, with 65 percent of the state’s LSRs being independent. Nationally, independent operators make up 42 percent of the LSR segment.

Naturally the states with the largest populations, such as New York, California, Texas, and Florida, have the highest volume of restaurants. When combined, these four states contain 36 percent of the total number of restaurants in the United States.

In terms of total number of units, the top five most popular simplified menu types nation wide are Varied, Pizza Pasta, Sandwich, Mexican and Hamburger, in that order, accounting for 55 percent of the restaurants nation wide.

“The Restaurant Unit Report provides a easy snap shot of what types of restaurants flourish in each state,” said Catherine Kearns, General Manager at CHD Expert The Americas. “This is especially valuable for suppliers who want to focus their efforts on certain markets or menu types. Furthermore, our recent introduction of franchisee data into our Easy2FIND platform, now gives unprecedented visibility into which chain restaurant are franchise owned. This intelligence is invaluable for both suppliers and chain restaurants who are looking to expand their territory.”

Is Dining Out Dimming Out?

A new study released by AlixPartners posits that the turbulence in the chain-restaurant industry of late — from underperforming results to an uptick in bankruptcies to renewed shareholder pressures — might not be just a blip but rather a sign of structural changes besetting the industry, and that the industry right now faces a defining moment. The study, which includes an in-depth survey of more than 1,000 U.S. consumers, examines a wide array of challenges and opportunities that, if properly addressed, might allow industry players to stay ahead of the big changes fundamentally altering the industry. The areas of the challenge and opportunity include technology, delivery, labor costs and growth.

High-frequency diners who patronize fast-food and fast-casual establishments at least twice weekly intend to cut back their visits by 8 percent and 13 percent, respectively, over the next 12 months

- Among those planning to dine out less in the coming 12 months, the most-cited reason, picked by 50 percent as one of their choices, was “saving money” – with 32 percent percent of those planning to spend that money on travel and 31 percent on “personal services”

- 56 percent say the top reason they choose ready-to-eat meals from convenience or grocery stores is because the meals are cheaper

- 74 percent say they order delivery from the same establishment routinely, with over half of those citing a lack of other options as the reason; yet only 8 percent using delivery prefer third-party services

- 58 percent say they agree with the movement for higher worker wages; however, those not willing to pay a bigger restaurant tab to support the movement rose to 16 percent, from 13 percent a year ago

- Traditional casual-dining topped the list of restaurant types consumers would like to see open more locations, picked by 37 percent – representing a possible growth opportunity

The study finds that 57 percent of consumers polled plan to dine out the same number of times in the next 12 months as in the previous 12, the same percentage who said that in a similar AlixPartners survey of a year ago. In addition, the average spending per meal reported by consumers in the survey for the past 12 months, $15.38, was the highest in AlixPartners’ nine-year history of conducting such surveys and, moreover, those surveyed said that over the next 12 months they plan to spend even a bit more, $15.43 per meal.

However, this year’s survey also uncovered big anticipated cutbacks, including among higher-frequency diners, the kind most coveted by the industry. For example, diners who patronized fast-food and fast-casual establishments at least twice weekly intend to cut back their visits by eight percent and 13 percent, respectively, over the next 12 months, according to the survey. At a more granular level, those polled said they plan to cut back their fast-food meals to 4.11 per year, down from 4.37 reported for the prior 12 month; their fast-casual meals to 2.93, vs. 3.01; their convenience-store meals to 3.65, vs. 3.71; and their ready-to-eat meals from grocery stores to 2.98, vs. 3.16.

Meanwhile, among those who said they plan to dine out less in the coming 12 months, the most-cited reason, chosen by 50 percent as one of their choices (of 16 available), was “saving money.” (That compares with 44 percent who cited “want to eat healthier” as one of their reasons to cut back on dining out.) And among those planning to dine out less in order to save money, the most-cited use for that saved money was “travel experiences,” picked as a reason by 32 percent of respondents. In addition, and perhaps unsurprisingly, the type of non-restaurant establishment chosen by consumers in the survey as most in need of dining upgrades was hotels, picked as a choice by 24 percent.

The survey also found big differences between what Millennials and Baby Boomers plan to do with the money they save by dining out less often. While the largest percentage of Baby Boomers, 47 percent, said they intend to put that money toward their retirement, that largest percentage of Millennials, 46 percent, cited “personal services,” which was defined to include things like hair and nail services, dry cleaning, housekeeping, etc. (For Baby Boomers, the comparable number was just 29 percent.) In addition, 26 percent of Millennials cited “education” as the intended use for that money, which, says the study, could well be taken to include the burden of paying off already-incurred student loans.

Adam Werner, managing director at AlixPartners and co-head of the firm’s restaurant, hospitality and leisure practice, said, “While lower fuel prices have helped operators by putting more money in consumers’ pockets, that’s become a two-edged sword as cheap gas and the lowest air fares we’ve seen since the recession seem to be enticing consumers to allocate at least some of their restaurant spending on travel and other experiences. Meanwhile, the all-important Millennial consumer, enabled the most by social media and other technologies that allow them to stay in close touch with friends even when they’re traveling, is the cohort most fundamentally shifting spending to experiences. Clearly, the challenge for the industry is to reinvent the ‘restaurant experience’ in order to compete with all the other experiences out there today.”

Technology: A “Mixed Bag”

When it comes to technologies in and around the restaurant and foodservice industry, the AlixPartners study finds that not all high-tech is either created equal or is of equal value to all consumers. For instance, more than twice as many Millennials as Baby Boomers in the survey, 42 percent vs. 18 percent, said they find technologies “very” or “extremely” influential to their decision to dine out. By the same token, though, mobile technologies appear to be slow to catch on, as 42 percent of respondents reported that they’ve never used mobile technology for dining-out. In fact, according to the survey online ordering and free Wi-Fi inside the eatery still remain the top-two technological influencers for diners, chosen as being “very” or “extremely” influential by 40 percent and 35 percent of respondents, respectively.

A similar story can be told for loyalty programs, digital and otherwise, where there is apparent slow consumer adoption as well. Only 19 percent of consumers in the survey said loyalty programs are “very” or “extremely” influential in their decision where to dine out. (However, that does represent a 5-percentage-point increase over the results in AlixPartners survey last year.) Meanwhile, 40 percent of consumers in this year’s survey said they haven’t joined a loyalty program, about even with the 42 percent in last year’s survey. However, those who are loyalists appear to be using more programs regularly, with 36 percent of respondents saying they are using two or more programs regularly, up 5 percentage points from last year’s survey results.

“Technology continues to be a mixed bag in the restaurant industry,” said Eric Dzwonczyk, managing director at AlixPartners and co-head of the firm’s restaurant, hospitality, and leisure practice. “There still doesn’t appear to be a lot of consumer ‘pull’ for many technologies, as food quality and price trump everything else. On the other hand, though, Millennials generally crave new technologies, so going forward the challenge may be how to balance diverse technologies preferences across consumer groups, without compromising service and operations along the way.”

Delivery: A Holistic Approach Is Best

A technological divide between Boomers and Millennials is apparent as well in meal delivery, says the AlixPartners report. Fifty percent of Millennials in the survey said they’re most interested in the availability of call-in-advance delivery; by comparison, 46 percent of Baby Boomers said they prefer traditional, “in-the-moment” delivery. The study further suggests other dichotomies in consumers’ attitudes towards delivery.

For instance, nearly three-quarters (74 percent) of consumers in the survey said they order delivery from the same eating establishment routinely, with more than half (53 percent) of that number citing as the reason “lack of good delivery options near me.” Plus, the survey finds consumers saying that they’d like to see more delivery options across multiple restaurant segments, with 38 percent of respondents picking as an option that they’d like more offerings from traditional casual-dining outlets, 37 percent saying so about fast-casual outlets and 34 percent saying it about fast-food outlets. However, says the study, companies responding to this demand by partnering with third-party providers should proceed carefully. Among those surveyed who order delivery, 71 percent said they prefer to get delivery directly from the restaurant, while only 8 percent said they prefer it through a third-party intermediary.

Meanwhile, according to the survey, the top two factors affecting the decision to order delivery from a restaurant are food quality, picked as a top influencer by 63 percent of those surveyed, and price of the food, chosen by 57 percent. Both, notes the study, are very much restaurant-controlled factors.

The study also notes that consumers seem to be quite aware of the price gap between restaurants and meals from grocery or convenience stores, emphasizing the importance of price-competitiveness in delivery. In the survey, 56 percent of respondents who choose ready-to-eat meals from convenience or grocery stores over restaurants said their No. 1 reason is because the latter meals are cheaper. Their own convenience came in second, picked by 22 percent of respondents.

“All the companies today putting investments into the third-party and other delivery programs might want to step back a bit and look at their operations holistically, with an eye on packaging and available technologies as well as delivery,” said Kurt Schnaubelt, managing director at AlixPartners and co-head of the firm’s restaurant, hospitality, and hospitality practice. “The challenge is to thoroughly understand how well your food ‘travels,’ and to maintain as much control as possible over the entire process.”

Higher Wages: Consumers Sympathize, But Don’t Necessarily Want to Pay

With more states adopting a higher minimum wage and other wage-increase movements afoot in the country, the AlixPartners study also sought to gauge consumers’ opinions today on the topic. In this year’s survey, 58 percent said they agreed with the movement for higher worker wages, up from 50 percent in last year’s survey. However, those saying they’re not willing to pay more at the restaurant to support the movement rose to 16 percent, up from 13 percent in last year’s survey.

Growth: “Zealously Exploit the Opportunities That Do Exist”

In general, the AlixPartners study describes an industry whose growth prospects today appear not to be as strong as in recent years, and that coming off a 2016 in which same-store sales were down for all major restaurant segments except quick service, while menu prices remained flat and labor as a percentage of revenue spiked upward.

However, despite that, the report pinpoints areas of potential growth going forward. For example, despite same-store-sales growth of only 0.8 percent in the casual-dining segment in 2016, what AlixPartners calls the traditional casual-dining segment (restaurants like Applebee’s, Chili’s, Olive Garden and Red Lobster) was the top vote-getter among restaurant types of which consumers would like to see more locations opened in the U.S., with 37 percent of those polled picking that segment as one of their choices. That was followed by what AlixPartners calls the traditional family-dining segment (restaurants like Bob Evans and Cracker Barrel), which was chosen by 34 percent, and the fast-casual segment (restaurants like Chipotle and Panera), chosen by 34 percent. Interestingly, notes the study, these results come on the heels of reports of significant over-capacity in the casual-dining segment.

“These findings beg the question of whether casual-dining and other players have put too much focus on bringing down prices, offering lunch, flooding the menu with healthy options, etc., in their efforts to compete with fast casual, eroding the opportunity for their own ‘special-occasion’ dining experience,” said Werner. “Clearly, there is still room for indulgences by diners at almost every segment level. The challenge for operators is to zealously find and exploit the opportunities that do exist.”

The report also uncovers an intended uptick in visits toward full-service establishments. In the survey, consumers visiting fine-dining establishments two to four times monthly said they expect to increase visits in the next 12 months by 20 percent — which, says the study, could be signs of both a growth opportunity for fine dining and of the aspirational intent of diners at all levels. In addition, the survey shows that when it comes to a desire for an expansion in locations, Millennials prefer fast casual over traditional casual dining (41 percent for fast casual vs. 33 percent for traditional casual dining). And for what AlixPartners calls specialty fast-casual concepts (restaurants like Shake Shack, Freshii and Blaze Pizza), which have seen significant growth over the past few years, the gourmet-burger concept was the No. 1 restaurant type consumers said they would like to see expand, chosen among the top three picks by 35 percent of those polled.

The AlixPartners survey also found that a modern or renovated look for a restaurant was near the bottom of attributes consumers said they cared about when ordering delivery, with only nine percent picking it as one of their important items. This, notes the study, perhaps suggests another opportunity for chains, specifically those looking to squeeze incremental profit from dated establishments.

Additionally, the AlixPartners report explores such things as regional and generational cuisine preferences, health-and-wellness issues and business issues such as industry profitability, stock-price performance and M&A outlook. The AlixPartners study included a survey taken Feb. 14-16 of 1,008 adults over age 18 from all major regions across the United States.

Restaurant Struggles are Real

Restaurant struggles continued in March as sales and traffic again declined year-over-year. Same-store sales were down -1.1 percent while traffic dropped -3.4 percent. March’s results were disappointing for an industry desperately trying to reverse performance trends; sales have been negative in 11 out of the last 12 months.

However, March did represent an improvement versus the prior month. Although still negative, sales improved by 2.5 percentage points compared to February. Traffic also improved by 1.6 percentage points. This insight comes from data by TDn2K™ through The Restaurant Industry Snapshot™, based on weekly sales from over 26,000+ restaurant units and 145+ brands, representing $66 billion dollars in annual revenue.

“March sales were expected to be somewhat better than February due in part to the catch-up of tax refunds that were initially delayed in February,” commented Victor Fernandez, Executive Director of Insights and Knowledge for TDn2K. “In addition, the industry likely benefitted from the shift in the Easter holiday, which fell in March in 2016. For the largest segments (quick service and casual dining), this holiday represents a potential loss of sales.”

“The fact that sales were still negative in March given these tailwinds highlights the challenge chains have faced since the recession. Factors like restaurant oversupply and additional competition for dining occasions continue to take their toll on chain traffic.”

Quarterly Results

With same-store sales declining -1.6 percent, the first quarter of 2017 was the fifth consecutive quarter of negative results. The last time the industry experienced a similar period was in 2009 and the first half of 2010, as the economy began recovery following the recession. Furthermore, the first quarter of 2017 followed a very disappointing -2.4 percent sales drop in the fourth quarter of 2016, highlighting the difficult operating environment currently facing many operators.

Unfortunately, same-store traffic dropped another -3.6 in the first quarter, consistent with the average -3.4 percent quarterly declines experienced since the beginning of 2016.

Average Guest Checks

The growth rate in check average continues to trend down slowly. For the first quarter of 2017, the average check was up 1.9 percent, somewhat lower than the average 2.3 percent growth reported for 2016. This is likely the result of brands relying more on promotions and conservative menu price increases in response to continual declines in traffic.

Industry Segment Results

As has been the case in recent quarters, segments with the highest and lowest average check experienced better results. The strongest performance in the first quarter came from upscale casual, followed by fine dining and quick service. It is important to mention that fine dining and upscale casual are among the segments most negatively impacted by the shift in Easter.

The weakest segments in the first quarter were family dining and fast casual. Family dining concepts were also among the most negatively affected by the Easter shift.

Despite continual sales slippage, there appears to be some positive news for casual dining. In 2015 and 2016, the segment trailed industry averages by roughly -0.7 percentage points. Although still negative, that gap to industry was only -0.1 percentage point in the first quarter. Casual dining has actually outperformed industry results in six of the past eight weeks. Conversely, over that same eight-week span, fast casual has trailed industry benchmarks six times.

The Restaurant Workforce

Finding enough qualified employees to keep restaurants fully staffed persists as a primary concern for restaurant operators. This is mainly due to restaurant turnover rates continuing to skyrocket while the labor market is at or near full employment. Turnover for restaurant hourly employees as well as managers increased again during February according to TDn2K’s People Report™. These rates are currently higher than they have been in over ten years and rising.

Restaurant brands are finding they need to offer a compelling reason for why employees should leave their current employment and come work for them.

Even if wages have been increasing slowly in recent years, this is expected to change soon as the labor market continues to tighten. In fact, according to a recent survey by People Report, about 80 percent of restaurant companies reported having to offer additional financial incentives to attract candidates in tough recruiting markets. In most almost all cases, those incentives take the form of higher base pay.

Restaurant job growth year-over-year has been slowing down in recent months and is now negative, likely a combination of the pace of new restaurant openings also slowing and staffing levels decreasing due to labor market challenges as well as conscious decisions to control costs. About 60 percent of restaurant brands tracked reported lower employee counts during February of 2017 than a year ago. This may not be good news for service scores and guest satisfaction.

This first quarter of 2017 seems to be consistent with 2016 as the industry chugs along and the rest of the economy gradually improves. We continue to seek the answer to “is our industry winning its share of the wallet in the economy overall and share of stomach in the overall food and beverage industry,” asks Wallace Doolin, Chairman and founder of TDn2K. “First quarter results would say that we are not winning our share so far this year. Our research does show there are real winners with impressive results. These “Top Box” performers are across the segments, size and ownership of the brands. Brands investing in the customer experience and the employee experience with technology and staff development are stealing share to grow their businesses.”

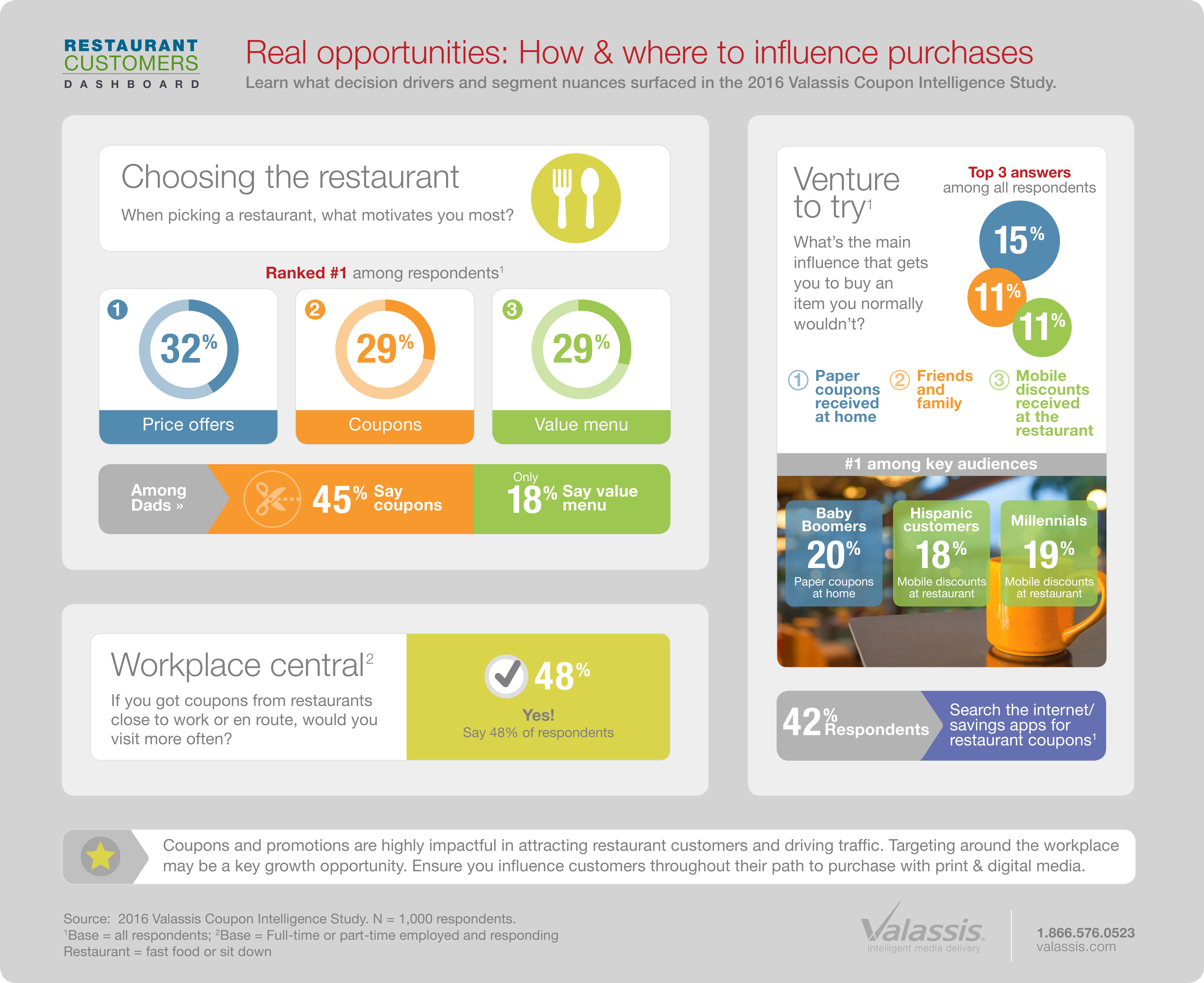

Coupons Drive Traffic

A recent study by Valassis found that coupons and promotions are highly impactful in driving restaurant traffic and customer engagement. According to the Valassis Coupon Intelligence Study, when choosing a restaurant, 32 percent are most motivated to select a location based on “price offers.” In addition, coupons and “value menus” have equal influence (29 percent each), reflecting the importance of tangible deals on driving dining out decisions. Also, 48 percent of employed survey respondents said they would visit a restaurant close to or on their way to work more often if they received coupons.

If restaurateurs and marketers aren’t tuned in to these types of insights, they are missing out on a sizable opportunity and may be underestimating the importance of engaging consumers with relevant messages.

“Consumers expect ready access to deals at home, work and on the go as they look for ways to save money and make dining out affordable,” said Curtis Tingle, chief marketing officer, Valassis. “The right deal, at the right time can activate a consumer who may not have been considering a restaurant otherwise, demonstrating the need to offer value at these influential moments along the path to purchase.”

Additional key restaurant findings from the Valassis Coupon Intelligence Study include:

- 45 percent of dads surveyed said they are most motivated by coupons when selecting a restaurant;

- 42 percent of respondents search the internet/savings apps for restaurant coupons; and

- 15 percent of consumers said paper coupons received at home are the main influence for buying a menu item they normally wouldn’t, while 11 percent said mobile discounts received at the restaurant are the main influence on this decision.

GPO Affiliation Growing

Nearly 40,000 independent restaurant operators are now affiliated with Group Purchasing Organizations (GPOs) and that number is only expected to grow. According to Dining Alliance, the use of GPOs is expected to rise because of the cost savings they provide to independent restaurant operators.

For example, Dining Alliance saw a 67 percent increase in its operator membership from 2014-2016, up from 13,000 to 21,000, respectively. This enabled the company to save its members in excess of $19.8 million in 2016 with a total of $4.3B in buying power.

“GPOs like ours level the playing field in an industry where large-scale chains often get better pricing. This gives independent operators the ability to run successful businesses in spite of today’s highly competitive market,” said John Davie, founder and CEO, Dining Alliance.

GPOs serve a 3-legged stool of stakeholders: operator members, contracted manufacturers and distributors. The GPO’s role is to keep the stool standing while advocating fairly for all, but most fairly for the operator member. Manufacturers want access to members (to supply products at GPO prices) and distributors need profitable relationships with both.

“Balancing the stakeholder stool is hard work. GPOs function in a complicated, messy supply chain where data is king, but not of royal pedigree. The lack of UPCs – Universal Product Codes – in foodservice handicaps the entire supply chain by forcing trading partners to create their own systems,” said Barry Friends, GPO and food service distribution expert, and partner with food consulting firm, Pentallect. “That’s a modest problem for giants like Tyson or Sysco, but individual operators at the end of the chain are ill-prepared to manage the vagaries.”

That is why GPOs have developed systems to unscramble the messy data and enable participants to benefit from each other’s contributions. They help members save money and show manufacturers where they can sell their products.

“That often creates friction with distributors since what’s good for one might not seem equally as positive for another. As advocates for independent operators, GPOs confront trading partner friction every day. And while everyone wants the best possible slice of the economic pie, the operator who buys the remaining portion needs to be able to stay in business,” Davie said. “If supermarkets operated like food service distributors, consumers would write to Congress for relief.”

Consumers Tempted by Specialty Foods

Sales continue to grow as Americans embrace specialty food and beverages. The industry is taking its place as an integral player with traditional and non-traditional specialty food retailers, foodservice operators, and distributors.

The Specialty Food Association’s (SFA) annual State of the Industry report examines the vibrant $127 billion-dollar industry in detail. Largely fueled by small business growth, total sales jumped 15 percent between 2014 and 2016. Growth is also driven by product innovations and wider availability of specialty foods through mass-market outlets. Sales through foodservice increased 13.7 percent to $27.7 billion as U.S. consumers make specialty food a regular part of their away-from-home meal purchases.

“Consumer preferences for specialty food products are growing at double digits, outpacing mainstream food staples.” said Phil Kafarakis, President of the Specialty Food Association. “The products our members create appeal to consumers looking for authentic tastes and foods with fewer and cleaner ingredients.

“Consumers are also making purchases wherever they happen to be, changing the retail food environment. The eagerness of all retailers including mass market, e-commerce, and foodservice to capitalize on these consumer trends is transforming the marketplace. Our research indicates that accelerated growth will continue and one of the things we’ll be doing at SFA’s 2017 Summer Fancy Food Show in June will be further exploring the projections we have for the future.”

Top trends identified in this year’s SFA research include:

- Sales Growth – Online Accelerates, Traditional Slows – while growth at retail and foodservice have slowed – up only 5.5 percent versus 9.1 percent in 2015, growth in third party e-commerce and direct-to-consumer websites have gained ground, accounting for almost 36 percent of sales

- Retail Channels Heating Up – Millennials, one of the top growing consumer segments, buy specialty food wherever they shop. This trend has helped drive sales in multi-unit grocery and mass merchants, where growth outpaced that of natural or specialty chains for the first time

- Center Store Alive and Well – Grocery, shelf-stable specialty foods accounted for 61 percent of the total specialty food market in 2016 ($36.2 billion). Strong growth performance was seen in categories like wellness bars and gels, and nut and seed butters

- Shift to Sustainable – Close to 40 percent of manufacturers produced sustainable products, up 22 percent from last year. Among retailers, sustainable products accounted for 16 percent of product sales. Along with non-GMO, the supply chain predicts sustainable will be the claim most interesting to consumers in the next three years.

Consumers are especially focused on specialty foods in the refrigerated sections. Categories with the biggest sales growth in this area include refrigerated juices and functional beverages up 30.7 percent, refrigerated lunch and dinner entrees up 33.0 percent, and yogurt and kefir up 27.2 percent.

Brits are in Love with Coffee

Visiting coffee shops is a ritual that many Brits routinely adhere to, as new research reveals Britain’s coffee shop culture is full of beans. According to Mintel research, the U.K. coffee shop market has enjoyed its biggest period of growth since 2008, when the market was valued at £2.2 billion. Over the last five years, the market rose by 37 percent, up from £2.4 billion in 2011 to reach an impressive £3.4 billion in 2016. What is more, between 2015 and 2016 sales increased a spectacular 10.4 percent – the biggest year-on-year boost witnessed in the last five years.

Over the next five years coffee shop sales are forecast to jump a further 29 percent, reaching a heart-stopping £4.3 billion.

It seems the market is brewing up for further success, as over the next five years coffee shop sales are forecast to jump a further 29 percent, reaching a heart-stopping £4.3 billion.

Brits’ insatiable appetite for coffee is highlighted by the fact that two thirds (65 percent) of all Brits have visited a coffee shop in the past three months. Coffee shop usage peaks among consumers aged 16-24 (73 percent). However, in a space traditionally dominated by specialist coffee retailers, it is notable that as many as 44 percent of Brits buy their hot drinks from non-specialists.

Overall, just one fifth (19 percent) of the nation do not drink tea, coffee or other hot drinks out of the home.

“Britain’s appetite for coffee shops continues, said Trish Caddy, Foodservice Analyst at Mintel. “Much of the growth we’ve seen in recent years is driven by habitual coffee drinkers and the continually increasing number of coffee retailers that are now ubiquitous on British high streets. A raft of non-specialist venues that feature barista-style coffee on their menus with takeaway functions are grabbing a slice of the coffee shop market. In the future, the top end of the market will continue to face intense competition from big pub chains, fast food chains and bakery shops that have now encroached on the coffee shop market, competing in terms of price, convenience and even geographical reach.”

Mintel research reveals an environmentally caring side to Britain’s coffee drinkers. Almost nine in 10 (87 percent) coffee drinkers try to dispose of their packaging waste in recycling bins. Some six in 10 (58 percent) coffee drinkers would like coffee shops to offer a discount to customers using their own travel mugs. Furthermore, four in 10 (40 percent) coffee drinkers say they do not mind being charged extra for hot drinks served in 100 percent recyclable coffee cups, and 30 percent would prefer to pay for filtered water instead of buying bottled water.

“The concerted efforts of coffee shops to cut down on coffee cup waste, following the recent documentary Hugh’s War on Waste, puts them at a competitive advantage by highlighting the fact that the sector as a whole feels obliged to be more ethical, ” she noted. “Recycling companies and packaging suppliers are making inroads by innovating in systems to recover and recycle existing materials, such as placing recycling bins in branded coffee shop chains as a collection point.”

Despite U.K. consumers’ love of coffee shops, for some, the draw of the kitchen remains too tempting. Half (51 percent) of coffee drinkers prefer to drink hot drinks at home rather than out-of-home, including 55 percent of men and 47 percent of women.

“The fact that half of coffee drinkers prefer to drink hot drinks at home could suggest that the range of beverages for at-home consumption may, in fact, be so well-established in the retail channel that more consumers can now recreate the coffee shop experience without having to leave the comforts of home,” she concluded.

A Chocolate for All Seasons

As chocolate lovers across the globe prepare to indulge in Easter treats, new research from Mintel reveals that seasonal launches accounted for one quarter (25 percent) of global chocolate new product launches in 2016, the biggest area of chocolate new product development (NPD) according to Mintel Global New Products Database (GNPD). In 2016, some 28 percent of seasonal launches globally were positioned for Easter, highlighting the ongoing popularity of eggs, bunnies and other chocolate treats. Those countries accounting for the most Easter chocolate innovation include Brazil, which accounted for 14 percent of global Easter chocolate product launches, France with an 11 percent share and South Africa with a 10 percent share.

At home, last year Brits spent a delicious £374 million on Easter confectionery. Mintel research reveals that confectionery continues to drive Easter purchases in the U.K. with 49 percent of Easter shoppers buying chocolate gifts in 2016. What is more, expenditure on confectionery accounted for approximately 68 percent of all Easter product spending.

Overall, launch activity in the confectionery category was somewhat restrained in 2016. The number of chocolate confectionery launches globally grew by just 3 percent between 2015 and 2016.

Marcia Mogelonsky, Director of Insight, Mintel Food and Drink, said: “Our research shows that seasonal chocolate tops all chocolate new product development, a testament to the popularity of seasonal treats among consumers across the globe. This reflects the fact that these products are typically bought to help celebrate holidays or special occasions. With this in mind, seasonal chocolate is somewhat immune to recessionary pressures as these products are bought on an occasional basis.”

“In countries where Easter is celebrated, there has been a broad range of new chocolate products coming to market. Easter egg innovation is especially interesting as manufacturers experiment with a range of products, from sweet to savoury. In 2016, the U.K. market saw growth in Easter treats in terms of both volume and value; however, value growth was highest, suggesting consumers may be investing in slightly more premium chocolate products as brands increasingly expand their offer,” she added.

When it comes to chocolate spend per head, the U.K. is top of the leaderboard. In 2016*, the average Brit indulged in 8.61 kg of chocolate (per capita). This was followed by Switzerland with 8.59 kg (per capita), Germany with 8.32 kg (per capita), Russia with 6.57 kg (per capita) and Austria at 5.37 kg (per capita). The U.K. and Switzerland have been vying for the top chocolate spot for some years now. For example, in 2013, Switzerland reigned supreme with per capita consumption at 9.3kg. While the international appeal of chocolate is unquestionable, Mintel research indicates a change in consumers’ eating habits among the top five chocolate markets as per capita consumption in the U.K. remained flat between 2015 and 2016; in Germany and Austria it fell 1 percent (respectively); and in Switzerland, per capita consumption of chocolate confectionery was down 3 percent.

While the U.K. is number one in terms of per capita consumption, when it comes to volume sales the U.S. leads the way. In 2016*, the U.S. consumed a spectacular 1.3 million tonnes worth of chocolate, followed by Russia in second place at 979 thousand tonnes and Germany at 680 thousand tonnes. The U.K. comes in fourth place at 555 thousand tonnes and France in fifth place with 251 thousand tonnes.

In recent years, the chocolate confectionery market has continued to see growth, though at a very slow rate, and in some established markets volume sales declined between 2015 and 2016. In the U.S., U.K., Germany and France, sales were flat over the two-year period, while sales fell in Russia (-2 percent), Brazil (-6 percent) and China (-6 percent). The only markets among the top ten globally to see any growth were Poland (+2 percent) and India, which saw an impressive 13 percent growth increase between 2015 and 2016.

“Chocolate confectionery had an uneven year in 2016. Volume sales in developed markets remained flat, while the picture was a bit brighter in emerging markets where sales generally fared better. Our research reveals that changes in per capita consumption points to an important shift in consumers’ eating habits, as consumption of chocolate confectionery is flat or declining in the top five markets. The big issues revolve around permissibility and the blurring of lines between snacks and confectionery. Even though boundaries are fading, there is still something about chocolate confectionery that has remained constant. Chocolate is still a treat and, as something special, it typically gets a pass. While consumers may be looking for more healthy foods, they will trade health for indulgence when it comes to chocolate.” Marcia continued.

Proving chocolate lovers have a heart, interest in ethical products remains relatively strong, with 17 percent of new products claiming some sort of “ethical-human” positioning, which could include fair trade, Rainforest Alliance or some other independent “bean-to-bar” certification. Although still a small part of the category, accounting for less than 6 percent of global new product introductions in 2016, launches of chocolate confectionery with an organic claim increased 6 percent between 2014 and 2016.

Consumer demand is likely to be the major impetus for more conversion to organic offerings. In the U.S., 15 percent of chocolate buyers purchase organic products. In Europe, interest is uneven with 14 percent of Italian chocolate eaters considering organic to be an important factor when buying chocolate, compared with just 4 percent of Polish chocolate eaters.

Despite this, Europe represents the region with the majority of organic chocolate product launches over the past three years, according to Mintel GNPD. Germany leads, accounting for nearly one quarter (23 percent) of global organic chocolate product launches, followed by France at 11 percent. It appears that Germany is also a major market for all natural (7 percent) and no additives/preservatives (7 percent) chocolate product launches. Elsewhere in Europe, demand for healthier sweets is strong. In Spain, six in 10 (60 percent) sweet eaters say there aren’t enough healthy sweets available. This view is shared among sweet eaters in Poland and France (58 percent respectively), markets that are not as well served by better-for-you (BFY) confectionery.

“Providing organic cocoa is proving to be a challenge for the industry. In order to satisfy the growing demand, it will become necessary for more cocoa growers to switch to organic farming methods. As interest in healthy sweets continues to rise, the availability of chocolate that offers organic or all natural positioning will be desirable as consumers look for better-for-you options,” she concluded.

Brand Penetration

A new index from The NPD Group’s Checkout Tracking SM shows that some of the biggest names in retailing and foodservice have become fully woven into American life – reaching an extraordinary percentage of buyers at least once a year. Walmart, McDonald’s, and Target top the list with better than five out of six U.S. consumers shopping in 2016.![]()

The Checkout Penetration Index, based on millions of receipts from actual consumers across all retailers and restaurants, both online and in brick and mortar, takes a new approach to understanding market penetration and performance. The index is based on one simple question: “What percentage of all U. S. consumers bought at each store or restaurant?”

The biggest gainer among restaurants in the Top 25 was Chick-fil-A, which saw a five percentage point increase in penetration in 2016. The biggest gainer among retailers was Dollar Tree, which saw a 3 percentage point increase. Both Chick-fil-A and Dollar Tree have been expanding operations aggressively.

“The battle for every consumer dollar is heating up, and we must shift from studying what consumers purchase to how they spend their money,” said Marshal Cohen, chief industry analyst, The NPD Group, Inc. “Consumers spending on experiences is overlapping with their purchases of products, making every item and visit so important to competing in today’s rapidly changing marketplace.”

Checkout TrackingSM provides detailed information on consumer buying behavior, based on receipts for both online and brick-and-mortar retail purchases from the same consumers over time. Checkout Tracking delivers precise category, brand, and item-level purchase detail linked to buyers and their demographics, useful for analyzing competitive market baskets and identifying purchase patterns. Information is collected from more than 50,000 consumers from NPD’s receipt-harvesting mobile phone app and the scanning of more than five million in-boxes for e-receipts through Slice Intelligence.

Singles Dining Preferences

Grubhub and Tinder teamed up to uncover the dining preferences of today’s singles.

Results from a nationwide poll conducted by the two companies showed a significant divergence from longstanding dating stereotypes, as a new generation dominates the dating scene.

The poll of Tinder users found the following insights:

Today’s singles embrace their hearty appetites.

Q: Which dish do you prefer on a first date?

A: 62 percent of respondents prefer a heartier dish, whereas 38 percent prefer a lighter meal.

You don’t have to offer to pick up the bill to make the step to a second date.

Q: Would not offering to pay be a deal-breaker?

A: Only 36 percent of respondents would rule out a second date if the other person didn’t offer to pay and 64 percent said it would not be an issue.

Grubhub and chill make for the ideal third date.

Q: It’s your third date. What do you do?

A: 60 percent of respondents prefer to order in for a casual night in, whereas the remaining 40 percent prefer to dine out.

What’s mine is yours.

Q: Your date keeps stealing food off your plate. What do you do?

A: ‘Scowl,’ according to 31 percent of respondents in comparison to 69 percent of respondents who answered ‘share.’

Unless you can use chopsticks, don’t bother with sushi.

Q: Your date uses a fork for sushi. What do you think?

A: 56 percent of respondents thought, ‘it’s cringe-worthy!’ and the remaining 44 percent thought ‘it’s adorable’ to forgo the chopsticks.

“Partnering with Tinder allowed us to tap into the food-related dating preferences and practices of today’s singles,” said Barbara Martin Coppola, chief marketing officer of Grubhub. “We’re thrilled to be part of the new dating experience and it is heartwarming to see that Grubhub can play a role in the love story of couples nationwide, as people get to know a new partner over their favorite local cuisine, from the comfort of home.”

The poll surveyed more than 2,000 people across the U.S. via the Tinder app. Participants were surveyed on their food-related dating preferences. By choosing answers through Tinder’s signature ‘swipe left’ and ‘swipe right,’ these participants allowed Grubhub and Tinder to draw five key conclusions about the etiquette of food during the first three dates.

“Most first dates involve food, so partnering with Grubhub to learn more about how eating preferences affect compatibility was a perfect fit for us,” said Rosette Pambakian, vice president, global communications and brand of Tinder. “The findings are interesting and highlight the important role food plays in dating.”

What’s Tops with Teens?

Piper Jaffray Companies completed its 33rd semi-annual Taking Stock With Teens research survey, which highlights spending trends and brand preferences amongst 5,500 teens across 43 U.S. states.

Since the project began in 2001, Piper Jaffray has surveyed more than 150,000 teens and collected over 38 million data points on teen spending in fashion, beauty and personal care, digital media, food, gaming and entertainment.![]()

“While the overall spending environment has been challenging, we are seeing teen spending continue to shift more toward experiences—eating out, video games and leisure,” said Erinn Murphy, Piper Jaffray senior research analyst. “Share of fashion spending has moderated but we continue to see undisputed strength in athletic—Nike remains the No. 1 preferred brand and Adidas was the fastest-growing brand in our survey.”

Spring 2017 Key Findings

Spending & Shopping Behavior

- Overall teen spending decreased 2.4 percent year-over-year.

- Parent contribution to teen spend is at 63 percent, down from the survey’s 68 percent average.

- Food is the most important category within a teen’s wallet at 24 percent of spend, eclipsing clothing at 19 percent.

- Fashion share of wallet moved down from 38 percent to 36 percent.

- Teens’ favorite website is Amazon at 43 percent share—up 200 basis points year-over-year.

- For console video games, the percent of teens who plan to digitally download >50 percent of games increased to 45 percent for spring 2017 from 37 percent in fall 2015.

Brand Preferences

- Starbucks is the only public brand to maintain double-digit share across all teenagers; it tied this survey cycle with Chick-fil-A at 12 percent preference.

- Athletic is seeing no slowdown with 41 percent of teens citing an athletic brand as their preferred apparel brand—up from 26 percent last year.

- Nike is the No. 1 apparel brand at 31 percent share—up from 21 percent last year. Adidas, however, is the fastest growing brand in our survey across footwear & apparel.

- Fashion brands losing relevance with teens include Under Armour, Michael Kors, The North Face, Ralph Lauren and Vineyard Vines.

- 81 percent of teens expect their next phone to be an iPhone, which was up from 79 percent in fall 2016 and, more importantly, the highest we’ve seen ever in the survey.

- Disney films dominated the most anticipated movies list with No. 2 “Beauty and the Beast”; No. 3 “Star Wars: The Last Jedi”; and No. 4 “Guardians of the Galaxy Vol. 2” grabbing the top few spots. “Fast 8” is the No. 1 most anticipated movie.

Rising Demand for Online Alcohol Sales

New analysis by e-commerce analytics firm Profitero projects rapid growth for online alcohol sales globally and offers insights to brands preparing to capitalize on rising consumer demand. The report, How Alcohol Brands Can Tap the E-Commerce Opportunity.

According to Keith Anderson, SVP, strategy & insights at Profitero and author of the new report, “Plenty of factors point to increasing demand for alcohol sales online, and we know that tech-savvy consumers expect to buy beer, wine and spirits online or with the tap of a smartphone just as they do any other product. Alcohol looks set to be the next sector to be disrupted by the continued shift to digital.”

Among the insights featured in the report, which are supported by data from Profitero as well as interviews with executives from Drizly.com, a major brewing company and Nielsen, are:

- The factors driving online sales growth;

- Unique hurdles facing e-commerce alcohol sales;

- Online delivery models in the U.S. and globally; and

- Ten ways alcohol brands can play online.

“In today’s evolving digital market, e-commerce is the newest frontier within the beverage alcohol space,” said Danny Brager, SVP, beverage alcohol practice at Nielsen. “Given the complexity of distributing and selling of Alcohol in the U.S. overlaid with differences by state and category, the migration to online sales will follow a slower curve that many other categories. However, there is a universal truth that this is an opportunity that our industry needs to recognize and begin to plan for, now – especially as more and more consumers get comfortable with the idea and practicality of shopping online for some of their needs.”

Top Asian Restaurants

Given how difficult it is to get a reservation at this Roppongi restaurant, it is fitting that Chef Takashi Saito’sSushi Saito restaurant in Tokyo has taken the number one spot in Opinionated About Dining’s first Top 100+ Asian Restaurants List.

Unsurprisingly for OAD’s founder, Steve Plotnicki, Japan dominates the 200-strong list, with 137 restaurants featuring. 33 restaurants hail from Hong Kongand 11 from Singapore.

“I had originally planned on publishing separate lists for Japan and Asia. But after seeing the way Japan was underrepresented on the 50Best list of Asia, I decided that the best way to give the chefs in Japan the recognition they deserve was to publish a single list.”

A former apprentice at Sushi Kanesaka, Saito has perfected Kanesaka-style sushi with carefully chosen seafood, flawless execution, and extreme precision. His sushi always has a perfect balance of flavours between neta and well-seasoned shari, and every piece he places in front of his guests is the exact same size, shape and temperature. Given the level of consistency of the experience, and Saito’s ability to deliver impeccable morsels of sushi over and over again, we understand why some of our reviewers visit this restaurant three or four times a year.

The number two spot on the 2017 list goes to MatsU.K.awa, an introduction-only restaurant where the only way to get a reservation is to be invited by a regular. Considered by OAD’s reviewers to be the best traditional kaiseki restaurant inTokyo, Chef MatsU.K.awa’s restaurant excels in transforming the most pristine ingredients into masterpieces by combining simplistic yet impeccable flavors with elegant Japanese aesthetics.

On Ultra-Violet by Paul Pairet being voted third on the list, Steve Plotnicki said, “Given how cuisine has shifted away from molecular cooking to the more natural style of cuisine that is so popular today, it is good to see an experiential dining experience ranked so highly by our reviewers.”

2017 Top 100+ Asian Restaurants

1 Sushi Saito Tokyo, Japan

2 MatsU.K.awa Tokyo, Japan

3 Ultra-Violet by Paul Pairet Shanghai, China

4 Kyo Aji Tokyo, Japan

5 Den Tokyo, Japan

6 Miyoshi Kyoto, Japan

7 Tenzushi Kyomachi-ten FU.K.uoka, Japan

8 Ogata Kyoto, Japan

9 Kimoto Kobe, Japan

10 Mizai Kyoto, Japan

Meal Kit Stats

Meal kits are the latest and greatest on the food-prep scene, aiming to make meal time easier, healthier, and more convenient for consumers. The kits, which can be purchased in stores or ordered online for delivery, offer pre-portioned ingredients and recipe instructions for a meal to be cooked at home. A recent Harris Poll shows 1 in 4 adults have purchased a meal kit in 2016 (25 percent) and 70 percent of meal kit purchasers are still actively purchasing meal kits.

Meal kits are hitting a mark with consumers and delivering on key convenience and health trends in the marketplace today. Among meal kit purchasers, the top reasons for buying include saving time on meal planning (46 percent) and the short prep and cook time (45 percent). Saving time is such a critical factor that even 44 percent of those who are no longer actively purchasing meal kits say they would consider doing so again due to the time saved on meal planning.

These are some of the results of The Harris Poll® of 2,015 U.S. adults aged 18+ surveyed online between December 27 and 29, 2016, including 474 who have purchased a meal kit in the past 12 months either in-store or online.

Why buy?

Rounding out the top five reasons for purchasing are saving time on grocery shopping (37 percent), trying new recipes (36 percent), and the healthy recipes (34 percent). A majority of active meal kit purchasers agree that meal kit dinners are healthier than prepared foods from their local grocery store. Seafood-based meals may be one of the new recipes that meal kits encourage buyers to try as two-thirds of active purchasers say they eat seafood more often when purchasing meal kits (66 percent).

When it comes to the contents of the meal kits, a vast majority of active purchasers appear to be very satisfied. Over 9 in 10 each say they are satisfied with the quality of the produce in their meal kits (92 percent) and with how the fresh meat is packaged (91 percent). While healthiness is clearly important, when it comes to meats, 89 percent of purchasers say they would be satisfied with regular (i.e., not organic) meat.

Room for improvement

While the list of benefits is lengthy, there are also areas for improvement. A majority of active purchasers are looking to feed their sweet tooth as well, with 86 percent saying they would add dessert to their meal kit if the option was available. Among those who have purchased previously but are no longer doing so today, nearly half say that a low cost would influence them to purchase. Over one-third would also be influenced to purchase meal kits if they were available in their local grocery store.

So is this latest entry in the food-prep scene here to stay or just a passing fad? “Consumers wanting convenience is here to stay, and providing a full-meal solution clearly meets a need for consumers. There is ample opportunity for both delivery and in-store options to capitalize on that need,” said Meagan Nelson, associate client director of Nielsen’s Fresh Growth & Strategy team.

Butter is Better

Healthy oils and fats are trending, and the U.S. food industry might be butter—uh better—for it. For more than 30 years, there has been unrelenting advice from dietary guidelines to cut fat and saturated fat from the American diet. But such notions have soured overtime and mindsets are changing. In particular, Millennials and Generation Z consumers are the most inclined to view any type of fat not only as permissible, but as offering positive health benefits, according to Food Formulation Trends: Oils and Fats, a new report by market research firm Packaged Facts.

“This is the culinary revolution of the Instagram generation,” says David Sprinkle, research director, Packaged Facts. “These young adults are unencumbered by the low-fat crazes of the 1990s and 2000s, and do not have to overcome negative perceptions about fat in general. Instead, they are able to readily embrace and seek out specific plant-based and animal-based fats for their health benefits, including fat from avocados, olive oil, eggs, butter, and omega-3 rich fish such as salmon.”

Packaged Facts forecasts that over the next few years, the foods most successful with these younger consumers will be those that contain minimally processed fats and oils that are free of GMOs and may even be organic. The report found that millennial and younger consumers, in particular, seek to avoid overly processed foods and ingredients, potentially boosting the appeal of natural, unrefined oils. When more description is included, it is likely to indicate naturalness and less processing, such as “raw,” “virgin,” “extra-virgin,” “unrefined,” “expeller-pressed,” and “cold-pressed” rather than “hydrogenated,” “refined,” “fractionated,” and “solvent extracted.” For example, when it comes to dairy products, the natural, full-fat versions of butter, milk, and cheese are more likely to be sought out because they are more natural and less processed.

“Butter is reemerging because it gives a stellar performance as a familiar ingredient that facilities clean and simple ingredient labels,” says Sprinkle. “For Millennial and Gen Z consumers, the new normal is clean and simple labels.”

In addition, Packaged Facts expects the popularity of plant-based specialty oils to benefit from increased availability of lesser known types of oil and wider, more mainstream, distribution of those already having established appeal. For all plant-based oils, continued interest in unrefined, cold or expeller-pressed oil is anticipated. These characteristics are important to Millennials when it comes to selecting fats and oils for pantry-stocking, use in home-prepared dishes, purchased prepared and processed foods, as well as restaurant meals.

Pizza Trends

When it comes to pizza, bold flavors, customization and authenticity are three key trends that are top of mind for consumers. At the 2017 International Pizza Expo, the Wisconsin Milk Marketing Board (WMMB) showcased how chefs are using specialty cheese from Wisconsin to bring these elements to life and meet consumer demand with innovative pizzas.

Bold Flavors

As pizza consumers move away from thick crusts to flatbread pizzas with fresh, locally sourced ingredients, operators are combining specialty cheeses from Wisconsin to create unique flavor profiles. WMMB featured a Mediterranean-style pizza at the Pizza Expo topped with Klondike Cheese Company’s muenster and feta cheese, Kalamata olives and oregano. A buffalo and ranch cheese curd pizza was also highlighted, featuring Ellsworth Cooperative Creamery’s buffalo-flavored and ranch-flavored Wisconsin cheese curd crumbles, sour cream, breaded chicken and finished with scallions.

Customization

According to Technomic, 76 percent of pizza customers prefer build-your-own customizable options. This is especially true for millennials who like the freedom of putting an individual touch on their food. Operators who may have offered two or three choices of cheese in the past are expanding their options, including cheese varieties that haven’t traditionally been associated with pizza. For instance, swiss, burrata and gouda are three of the fastest-growing cheeses currently used on pizza, all of which can be sourced from America’s Dairyland.

“Pizzas need not be just mozzarella anymore,” said WMMB chef consultant John Esser. “The growing palate of America is looking for blends of Wisconsincheese that excite their taste buds. A 10 percent addition of say, aged provolone, on top of mozzarella, will make the flavor profile jump when it hits your mouth.”

Authenticity

Pizza consumers crave authentic, chef-driven specialty pies made with seasonal and local ingredients. Wisconsin dairy farms, 96 percent of which are family owned, have been helping produce many of those key ingredients for over 160 years. In the past two years, the specialty pizza category has increased by 4.6 percent (Technomic Q2 2014 – Q2 2016). This time period also saw a 64 percent increase in pizza menu mentions of Wisconsin cheese. Consumers want to know where their food is coming from, and will also pay a premium for it. WMMB research shows that an entrée pizza with Wisconsincheese commands a 14 percent price premium over the average price of other entrée pizzas.

Hot Trends in Hot Dogs

Like popcorn at the movies, hot dogs are the quintessential summer ballpark food, and the National Hot Dog and Sausage Council (NHDSC) estimates that baseball fans will consume nearly 19 million hot dogs and more than 4.1 million sausages during the 2017 Major League Baseball (MLB) season. The combined hot dog and sausage total could stretch from San Francisco’s AT&T Park to the new SunTrust Park in Atlanta, Georgia. The hot dog total alone would reach as high as 5,301 One World Trade Centers, the tallest building in the Western Hemisphere.

“Year after year, hot dogs continue to hit it out of the park at the concession stand,” said NHDSC President Eric Mittenthal. “As teams innovate to offer more food choices and inventive creations, one thing is certain: hot dogs and baseball are inseparable.”

The Los Angeles Dodgers can relish in victory as the team’s fans are once again projected to consume the most hot dogs, totaling more than 2.5 million. That is enough to round the bases at Dodger Stadium 3,434 times, and based on last year’s attendance, means that nearly 68 percent of fans at Dodger home games will eat a hot dog.

In a surprise upset, the Texas Rangers threw a curveball to claim second place, as fans are expected to consume more than 1.4 million hot dogs, representing a 17.2 percent increase over 2016. Batting third are the Cleveland Indians at 1,080,000 hot dogs, followed closely behind by the reigning World Series champions Chicago Cubs with 1,000,000 anticipated hot dog sales. The St. Louis Cardinals and Boston Red Sox round out the lineup of top hitters, with fans expected to consume more than 959,720 and 850,000 hot dogs, respectively.

The San Francisco Giants have defended their title as MLB sausage champions, with 475,000 expected sales. The St. Louis Cardinals once again stepped up to the plate to clinch second place with fans expected to consume 419,356 sausages. The Boston Red Sox, meanwhile, earned third place with Fenway Fans expected to eat 327,500 sausages this year.

It’s a whole new ball game at Miller Park, home of the world-famous Klement’s Sausage Race, where the MilwaU.K.ee Brewers have reclaimed their position as the only team in baseball that is expected to sell more sausages than hot dogs.

While there is no shortage of MLB rivalries, our survey finds that hot dogs bring all sides together, with numerous stadiums featuring the regional flavors of their competitors. Kauffman Stadium, home of the Kansas City Royals; Minute Maid Park, home of the Houston Astros; and Coors Field, home of the Colorado Rockies will sell a number of regional favorites including the Denver Dog, Coney Island Dog, Georgia Dog, Chicago Dog, Cincinnati Cheese Coney and New York City Dog.

The Los Angeles Dodgers, meanwhile, will offer different hot dogs based on their opponent each homestand, with specials that include the Chicago Dog, Philly Dog, Miami Cuban Dog, MilwaU.K.ee Dog and New York Dog.

The survey also reveals that the trend toward offering hot dogs and sausages from local area businesses is here to stay. Progressive Field, home of the Cleveland Indians, for example, will serve fans local favorites from Happy Dog. Fans at Nationals Park, home of the Washington Nationals, can enjoy food from area staples like Ben’s Chili Bowl and Haute Dogs and Fries, while Safeco Field, home of the Seattle Mariners, will sell nearby Fletchers hot dogs and Hempler’s sausages.

Some of the top 2017 MLB rookies include:

- Sunrise Dog: Royals fans can indulge on this hot dog topped with bacon, cheddar cheese, fried egg and white sausage gravy. Sold only on Sundays, fans shouldn’t feel too guilty to enjoy more than one.

- Harry The K’s Pastrami Sausage: Phillies fans should come hungry to eat this house-cured pastrami sausage topped with hickory-smoked bacon, red cabbage and tarragon mustard.

- The M.V.T. Dog: Also known as the Most Valuable Tamale, this new creation is not for the faint of heart. Rangers fans should come prepared to tackle this tamale that is filled with the famous 24-inch Boomstick hot dog, covered in chili and nacho cheese.

- Bloor Street Dog: Hot dog love knows no borders. Toronto Blue Jays fans can relish in this hot dog topped with butter chicken, chili-lime sour cream, a trio of Indian vegetables and fresh chopped parsley.

- Brunch Bloody Mary: This drink concoction features a skewer of sausage, egg, chicken and waffles, bacon and donuts served in a keepsake mason jar.

- Red Sox Triumph in Hot Dog Madness Bracket Contest

How Do You Say Caramel?

Werther’s Original celebrated National Caramel Day by asking caramel lovers nationwide how they pronounce their favorite treat: ker-uh-muhl or kar-muhl. The national survey results are in and ker-uh-muhl takes the sweet honors with 57 percent of Americans using the three-syllable pronunciation.

Caramel lovers nationwide shared how they pronounce “caramel” on National Caramel Day, April 5, by using #GreatCaramelDebate on Facebook, Instagram or Twitter.

The results of the survey uncovered regional trends in pronunciation, with ker-uh-muhl being the most popular pronunciation in the Northeast, South and West, and kar-muhl coming out on top in the Midwest:

Northeast

57 percent ker-uh-muhl

43 percent kar-muhl

Midwest

43 percent ker-uh-muhl

57 percent kar-muhl

South

64 percent ker-uh-muhl

36 percent kar-muhl

West

58 percent ker-uh-muhl

42 percent kar-muhl