According to a Recent Study/Survey … End-of-August 2017 Edition

23 Min Read By MRM Staff

Can you believe it’s nearly September? This edition of Modern Restaurant Management (MRM) magazine’s “According to a recent study/survey …” research feature includes the impact of a long weekend in the hospitality industry, debunking the retail apocalypse, catering in Saudi Arabia, U.S. wine consumption and the return to authenticity.

Long-Weekend Flu?

Customers planning to spend the unofficial last day of summer enjoying drinks and snacks on the patio should prepare themselves for longer wait times and diminished service. This is due to a predicted outbreak Long-Weekend Flu, an ailment unique to the service industry.

According to research by Toronto-based tech firm Staffy, 22 percent of service workers are planning to call in “sick” over the long weekend, leading to one of the most far-reaching cases of Long-Weekend Flu this century.

“It’s well documented that a higher-than average number of service workers come down with some sort of debilitating illness during three-day weekends, but fortunately Staffy has a proven remedy for the phenomenon,” said Peter Faist, founder of Staffy. “We have thousands of healthy contractors eager to fill in for these shifts while the permanent workers get much-needed rest.”

The survey also found some surprising additional stats among service workers:

- 56 percent of restaurant workers prefer to work a standard 9 to 5, Monday to Friday shift, despite far heavier traffic and tips evenings and weekends

- Nearly half of respondents (44 percent) would prefer to see tipping eliminated in exchange for a higher, predictable wage

- 62 percent of hospitality workers are part-time workers pursuing other interests

Caused by regular staffers calling in “sick,” or otherwise dropping shifts on very short notice in order to enjoy the summer’s last long weekend, Long Weekend Flu often causes substantial lost business while also subjecting patrons to long waits for tables, drink, food, and their checks, as establishments scramble to find temporary staff on short notice.

Americans Love Waffles

National Waffle Week starts September 3, and if you’re like eight in ten Americans who reportedly love the breakfast mainstay, ezCater has everything you need to know about what’s trending in the world of waffles.

Using data from actual orders placed through its network of 50,000+ restaurants and caterers across the country, ezCater looked at factors from top types of waffles being ordered, to the most waffle-crazed metros, and the top restaurants and caterers serving up the fare. Some of the findings include:

- Portland and Seattle love waffles: When looking at top cities based on waffle orders, Portland (847 orders with waffles) and Seattle (481 orders with waffles) claim the first and second spots on the list.

- People crave classics with a creative touch: The best waffle restaurants and caterers are those that have either perfected the classics (Belgian, chicken and waffles), or have gotten creative with toppings, like Nutella, bacon, and pecans.

- The best waffles are in Chicago: Babycakes Gourmet in Chicago is the top waffle joint on ezCater’s platform.

Top cities sorted by number of waffle orders:

- Portland, OR: Portland ranks number one in terms of all-time waffles order on ezCater. Businesses in Portland have ordered nearly 12% of all the waffles ever ordered on ezCater.

- Seattle, WA

- Boston, MA: Boston orders the largest quantity of waffles on the East Coast. Boston loves waffles so much, that the city’s businesses actually order the third largest quantity of waffles in the U.S., coming in just behind Portland and Seattle.

- Los Angeles, CA

- San Francisco, CA

- Chicago, IL

- Cincinnati, OH

- Houston, TX

- New York, NY

- Baltimore, MD

Most popular caterers for waffles on the ezCater platform

Babycakes Gourmet (Chicago, IL): The Chicago-based food truck carts around waffles, pancakes, and other breakfast foods in wacky, sweet and savory variations like Red Velvet, Sausage Cheddar, and Oreo Cheesecake.

Bru’s Wiffle (Los Angeles, CA): This family-friendly joint specializes in excellent chicken and waffles, as well as other bite-sized waffle creations — don’t place an order that doesn’t include a stack of infinitely poppable chocolate mini waffles. Oh god

Café Jolie (Oakland, CA): Sustainable, organic food is on the menu at Café Jolie, whose breakfast waffles include fresh, seasonal fruit, toasted nuts, and homemade whipped cream.

Voya Restaurant (San Jose, CA): Voya Restaurant puts a Latin-American twist on traditional breakfast dishes, like the Spicy Aioli Egg Sandwich. The waffle is served in a more classic style, but comes topped with locally grown berries and pure maple syrup.

The Waffle Window (Portland, OR): Truly a waffle lover’s paradise, The Waffle Window serves the breakfast pastry in countless different versions, from peanut butter chocolate dipped to ham and cheese.

Zinneken’s (Boston, MA): “Best Belgian waffles made by actual Belgians” is the slogan at this authentic Cambridge café. Its signature Belgian Sugar Waffles are made with imported pearl sugar from Belgium, which especially caramelizes in the waffle iron to yield a sweeter, more decadent end result.

Green Market Café (Tampa, FL): Choose Green Market Café for a diverse set of healthy, tasty breakfast options (including waffles!) that won’t leave you totally weighed down.

Church’s Chicken (Washington, DC): This iconic chicken spot serves the kind of thick, crispy, crunchy fried bird that you crave. Set over a chewy waffle, it’s a breakfast lover’s dream.

Corporate Caterers (Austin, TX): Corporate Caterers offers reliably high-quality fare with efficient, easy service. The breakfast options are a highlight, and include a Belgian Waffles & Egg Bar, where guests can choose between toppings like fresh strawberries, toasted sweet pecans, powdered sugar, and maple syrup.

Cast Iron Waffles (Charlotte, NC): The waffles at Cast Iron Waffles are made with brioche dough, the key to a fluffy, sturdy texture. You can even order sides of Nutella, maple butter, or vanilla for guests to have fun with their toppings.

According to ezCater’s data, these clever takes on the breakfast staple are growing in popularity across the country:

- Belgian Waffles

- Chicken & Waffles

- Mini Waffles (in regular and chocolate flavored)

- Waffle Sliders

- Flavored Waffle Sticks

- Churro Waffles

- Waffle Dogs

- Nutella Waffles

- Berry Waffles

Customer Visits Trending Downward

Customer visits to U.S. restaurants and foodservice outlets remained negative in the quarter ending June resulting in six consecutive quarters of weak traffic performance, reports The NPD Group, a leading global information company. The U.S. foodservice industry has not experienced six quarters in a row of no traffic growth since the recession of 2008-09. The average check at foodservice outlets rose by 2.6 percent — the largest increase in several years — reflecting higher menu prices.

The vast majority of consumers give restaurants fairly low ratings on affordability compared to other customer satisfaction attributes.

“No doubt the rising cost of a restaurant meal is weighing heavily on industry traffic performance,” said Bonnie Riggs, NPD Group restaurant industry analyst. “The vast majority of consumers give restaurants fairly low ratings on affordability compared to other customer satisfaction attributes.”

The slowdown in restaurant and foodservice visits is most prevalent at midscale/family dining and casual dining concepts. Midscale registered a 4 percent decline in traffic in the quarter compared to same quarter year ago. Casual dining visits dropped by 3 percent in the quarter, according to NPD’s CREST®, which daily tracks all aspects of how consumers use restaurants.

Visits also softened for quick service restaurants (QSR), which represent the lion’s share (83 percent) of industry traffic and has been the only driver of industry traffic growth for several years. QSR customer visits were flat in the quarter compared to last year but a steeper decline was offset by traffic growth at QSR hamburger and fast casual restaurants. The QSR hamburger category realized nearly 13 million more visits in the quarter than last year, and fast casual grew traffic by 77 million incremental visits.

In addition to QSR hamburger and fast casual restaurants, other industry bright spots in the quarter included the continued growth of morning meal visits, up 1 percent in the quarter over year ago, and foodservice delivery, up 2 percent. The quick service segment was primarily responsible for the uptick in morning meal visits. Delivery growth was entirely derived from four restaurant categories: QSR sandwich, QSR burger, midscale, and Asian.

“Although there were a few performance bright spots this quarter, these visit occasions are not large enough to move the industry in a positive direction,” added Riggs. “Operators will need to be critical in increasing prices and make sure that when they do raise prices the quality of the food and experience is commensurate with their customer’s cost.”

Debunking the Retail Apocalypse

U.S. retailers are opening 4,080 more stores in 2017 than they are closing and plan to open over 5,500 more in 2018, according to a new research report from IHL Group. The report, Debunking the Retail Apocalypse, was released today and is available here.

The research reviewed over 1,800 retail chains with more than 50 U.S. stores in 10 retail vertical segments. It found that for every chain with a net closing of stores, 2.7 companies showed a net increase in store locations for 2017.

“The negative narrative that has been out there about the death of retail is patently false,” said Greg Buzek, president of IHL Group. “The so-called ‘retail apocalypse’ makes for a great headline, but it’s simply not true. Over 4,000 more stores are opening than closing among big chains, and when smaller retailers are included, the net gain is well over 10,000 new stores. As well, through the first seven months of the year, retail sales are up $121.6 billion, an amount roughly equivalent to the total annual retail sales of The Netherlands.”*

Highlights of the research include the following:

- The total net increase of stores for 2017 is 4,080, including retail and restaurants. Core retail segments will see a net gain of 1,326 stores, while table-service and fast-food restaurants are adding a net of 2,754 locations. In total, chains are opening a net 14,239 stores and closing 10,123 stores.

- 42 percent of retailers have a net increase in stores, only 15 percent have a net decrease, and 43 percent report no change.

- The three fastest growing core retail segments are mass merchandisers such as off-price retailers and dollar stores (+1,905 stores), convenience stores (+1,700 stores) and grocery retailers (+674 stores).

- Specialty apparel retailers are seeing the largest number of closings, with a net loss of 3,137 stores. Yet, for every chain closing stores, 1.3 chains are opening new stores.

- When it comes to chains shuttering stores, only 16 chains account for 48.5 percent of total number of stores closing. Five of these chains (Radio Shack, Payless Shoesource, Rue21, Ascena Retail and Sears Holdings) represent 28.1 percent of the total stores closing.

“Without question, retail is undergoing some fundamental changes. The days of ‘build it and they will come’ are over,” added Buzek. “However, retailers that are focusing on the customer experience, investing in better training of associates and integrating IT systems across channels will continue to succeed.”

Debunking the Retail Apocalypse was underwritten by AT&T, Cayan, Fujitsu, Aptos, Level 10, Adspace, and Veras Retail. The research report began with the review of 2,400 retail chains operating in the U.S. from the IHL Sophia Data Service, then was narrowed down to 1,804 chains with 50 or more stores. The growth in stores were counted at net gain or loss per chain, and each retailer was evaluated if their net number of stores increased or decreased. If positive, IHL counted the net increase. If negative, it was counted as net decrease. Data was not calculated within a retailer’s portfolio. Thus, a retailer that opened 10 stores and closed two was counted as +eight.

The Power of Family Meals

- Family meals are beneficial. Numerous studies have found that eating with others, particularly family, is associated with healthier dietary outcomes for children and adults.

- Family meals usually fail to happen. Daily behaviors suggest that parents eat home-cooked dinners with their child or spouse only half the time (3.5 times out of 7 possible dinners each week).

- Barriers to family meals. The primary obstacle for missed family meals is differing schedules reported by 55 percent of adults living with children, 47 percent of adults living together without children).

- America’s changing families. Today’s eaters live in dramatically different household structures and habits from the traditional family that once revolved around married life and children.

- Honoring the Dinner Hour – to preserve the sanctity of dinnertime among Americans with intractable schedules even if it means reserving options for narrower windows of time.

- Shifting Dayparts – to modify the timing of social eating to breakfast considering that it might be easier for busy families to connect before the day starts when busy evening schedules persist.

- Making a Family of Friends – to encourage young adults living alone to connect with each other for home-cooked dinners.

Catering in Saudi Arabia

Saudi Arabia has seen growing number of tourist majorly for religious purpose which has facilitated growth in the hospitality sector. Furthermore, the government has taken initiative to develop the infrastructure in the country. This has led to growing demand in construction sector and hospitality sector which majorly includes Hajj catering and hotels.

Use of digital platform in the Saudi Arabia Catering Services Market has helped in making the whole process simpler, transparent and more effective. Major companies are using technology to monitor the procurement process to control the quality standards, manage inventory and storage facilities and reduce wastage by using appropriate equipments and proper estimation of food to be produced for a certain event.

Government authorities such as SFDA have laid down guidelines and regulations to monitor the quality of catering services provided in schools, hospitals and labour camps in order to avoid food poisoning and inculcate healthy eating habits.

Saudi Arabia Catering Services Market has seen development in the last five years with the implementation of Saudi Arabia 2030 and National Transformation Program which focused on developing the infrastructure of the country. As construction activities increased it aided the growth of catering services in labor camps. The industrial and hospitality catering sector has accounted for the largest revenue share in 2016. Growing population, need for the development of a robust transport network, government emphasis on the development of renewable energy infrastructure and strong growth of the non-oil sector have augmented the demand for housing, industrial/commercial construction. The industrial and construction sector has been dominated by expatriates who mostly remain alone. Such employees demand catering services for 3 meals a day at competitive prices. Religious cities such as Makkah, Jeddah and Madina receive millions of religious tourists every year that rely on catering companies for three meals a day during their stay in Saudi Arabia. With the advent of internet, customers are now more knowledgeable about different cuisines and are demanding a fusion menu. This has been supported by increased smartphone penetration which has made the process simpler.

U.S. Wine Consumption Increases

The U.S. wine market, the largest in the world, continued to show strength in 2016 growing 2.4 percent to 341.1 million 9-liter cases led by a 6.6 percent upsurge in the consumption of total sparkling wines, according to the Beverage Information Group’s 2017 Wine Handbook. A strong U.S. economy, employment and wage gains, and larger discretionary incomes all contributed to the category’s growth.

Total domestic wines accounted for 76.8 percent of the wine category, up slightly from last year. The number of U.S wineries also continued to grow, topping almost 8,300, up 4 percent. California, the largest wine producing state, continued to capitalize on the increasing popularity of its premium and super-premium wine segments in 2016. Wines produced in Oregon and Washington also continued to show promise as consumers are demonstrating their willingness to explore wine beyond the California segment.

The premiumization trend in the wine market has not slowed but rather continued to evolve in 2016. Consumers continued to seek premium and high-end brands to enjoy at home and in on-premise venues. Sales of wines priced under $10 weakened again this year with wines in the $10 to $20 range thriving. In fact, many major brands had trouble staying top of consumers’ mind as was also the case last year. Smaller brands are becoming more attractive as word of mouth and social media platforms create unique awareness that is not found in traditional advertising mediums.

Table wine grew to 309.4 million 9-liter cases, a 2.2 percent increase over 2015, as reported by the 2017 Wine Handbook. The champagne and sparkling wine category grew for its 15th consecutive year to 22.1 million 9-liter cases, up an impressive 7.8 percent. Domestic sparkling wine reached 11.9 million 9-liter cases resulting in a 5.2 percent increase in volume, continuing an eleven-year growth streak.

The Authenticity Trend

More consumers are seeking out food that is made with integrity and respect for culinary traditions… No matter what cuisine is being offered, consumers increasingly expect that food to be true to its roots and culture.

So proclaims a new white paper from Coast Packing Company, the West’s leading supplier of animal fat shortenings lard and beef tallow. The document – Return to Tradition: Renovate Your Menu with Authentic Ingredients — details how animal fat shortenings can improve profit margins and enhance flavor and quality, while meeting growing consumer demand for authenticity, health and sustainability.

“One simple, easy and economical way to increase the authenticity of many ethnic cuisines as well as American comfort foods is to switch from vegetable oils to natural animal fat shortenings, such as lard and beef tallow,” writes Coast Packing Corporate Chef Ernest Miller, author of the white paper. “In addition to enhancing the bottom line, heritage fats are on trend for flavor, wellness and sustainability.”

Underlying the Coast white paper are three lessons for the restaurant sector, Miller said:

- Consumers are demanding authenticity

- Animal fat shortenings enhance quality naturally

- Animal fat shortenings are more sustainable

“Consumers do not want insipid, watered down, banal versions of a cuisine; they want to embrace and celebrate that cuisine,” he said. “Rather than generic versions of a nation’s culinary arts, diners are seeking out more authentic, local variations – not just Mexican food, but Oaxacan dishes or other regional specialties. Even when the menu being presented mixes and matches elements of cuisines for nouvelle or fusion effects, diners assume that the ingredients will reflect the essence of the dishes that were the inspiration for the synthesis.”

As the Coast white paper explains, customers would rather a restaurant incorporate authentic ingredients and provide a faithful experience of a culture’s food than dispense the mere simulation of a dish: “And those who can provide patrons with an authentic experience earn their trust and build a relationship with their consumers for the long-term.”

According to Coast Packing CEO Eric R. Gustafson, this reverence for tradition isn’t simply a search for historical accuracy – it’s a quest for flavor. “There is a reason certain ingredients are traditional — they provide better taste and quality than the non-traditional alternatives,” he said. “That is how they became traditional in the first place. And with 95 years in the business, we at Coast know a little bit about tradition.”

To download a copy of the Coast Packing Company white paper, click here.

Michigan Restaurants Report Optimism

The Michigan Restaurant Association (MRA) released its second quarter research report tracking economic and demographic trends within the restaurant industry on a statewide basis. The survey, conducted by independent research firm Cleveland Research and distributed to MRA’s nearly 4,500 members, suggests improved sales in the second quarter and confidence that sales growth will continue the second half of the year.

Highlights from the Q2-2017 Trends Report include the following:

- Sales across Michigan restaurants increased by 3.2 percent in the second quarter of 2017, an improvement from the first quarter, but still behind 2016 growth rates.

- Optimism abounds as a robust 71 percent of respondents expect same-store sales growth to be better in the second half of the year.

- After 18 months of stable to deflationary food prices in the industry, costs appear to be increasing as survey respondents reported a .5 percent increase in food costs as a percentage of total sales.

Additional findings suggest a healthy Michigan economy, with unemployment rates plummeting below five percent, has made staffing a primary concern for restaurant owners. The lack of supply combined with significant industry demand is driving wage increases as labor costs continue to outpace 2016 figures for the second straight quarter.

“The restaurant industry in Michigan bounced back in the second quarter with year-over-year sales growth nearly doubling lackluster sales growth figures in the first quarter,” said MRA President & CEO Justin Winslow. “While this is great news, the industry is still under significant pressure from rising labor costs and what appears to be the end of flat commodities prices.”

Americans and Bread

- Grain foods pack more of a nutrient punch than a caloric one in adult diets. All grain foods contributed less than 15 percent of all calories in the total diet, while delivering greater than 20 percent of three shortfall nutrients – dietary fiber, folate, and iron – and greater than 10 percent of calcium, magnesium, and vitamin A.

- Grain foods fill critical nutrient gaps. All grain foods collectively are nutrient-rich and are sources for several shortfall nutrients and nutrients of public health concern. This includes dietary fiber, folate, magnesium, calcium, and iron.

- Explicitly, breads, rolls and tortillas and ready-to-eat cereals are meaningful contributors of dietary fiber, thiamin, folate, iron, zinc and niacin to the American diet of adults.

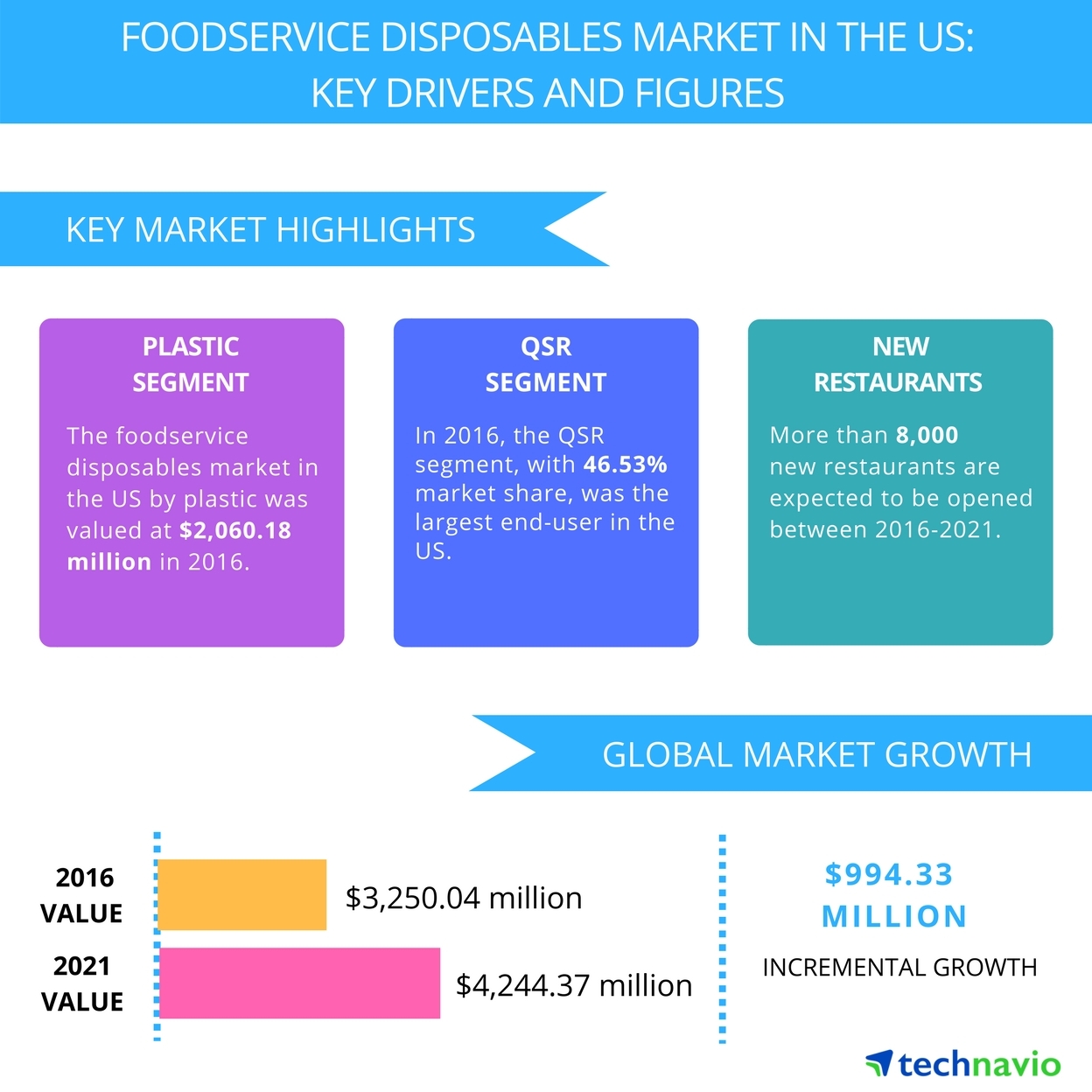

Foodservice Disposables Market

Technavio’s latest market research report on the foodservice disposables market in the US provides an analysis on the most important trends expected to impact the market outlook from 2017-2021. Technavio defines an emerging trend as a factor that has the potential to significantly impact the market and contribute to its growth or decline.

According to Manu Gupta, a lead analyst at Technavio for food serviceresearch, “The growth of the foodservice disposables market in the US will be driven by various factors, such as the growth of online channels for delivery of food and beverages. Increase in the number of international tourist arrivals will also drive the growth of the foodservice industry and the market for foodservice disposables.”

The top three emerging market trends driving the foodservice disposables market in the US market according to Technavio research analysts are:

- Use of UV-cured ink on disposables

- Increase in use of recyclable plastic for foodservice disposables

- Growing market for biodegradable foodservice disposables

Use of UV-cured ink on disposables

Most foodservice providers use foodservice disposables made from paper and plastic. These are cups, plates, trays, and containers have customized prints and designs, including the name and logo of the foodservice establishment. For instance, McDonald’s, Burger King, KFC, and Dunkin’ Donuts provide beverages in paper and plastic cups with custom prints on them. Similarly, leading cafés such as Starbucks and Tim Hortons also have their prints on their disposable cups for beverages.

Due to versatility and wide applicability, solvent-based inks are generally used by most manufacturers of foodservice disposables. However, solvent-based inks have downsides like they emit VOC and are harmful to human health and atmosphere. UV-cured ink contains little or no VOC because it does not contain heavy metals that can be harmful to humans and the environment. Thus, some foodservices disposables vendors have started using UV-cured ink with the objective of either reducing VOC or eliminating the need to report them. During the forecast period, it is expected that use of UV-cured ink will rise significantly and may drive the growth of the market.

Increase in use of recyclable plastic for foodservice disposables

Plastic is known for its property of slow degradation, which takes approximately 100 years to 1,000 years. This raises concerns among environmentalists as the plastic-based foodservice disposables segment has the largest market share in the foodservice disposables market in the US.

“Increasing focus on the benefits of recyclable plastic and waste management may encourage many vendors to enter such activities during the forecast period. For instance, Anchor Packaging recycles almost 100 percent of its raw materials, and its plastic-based foodservice disposables are made from PETE, which is the most recycled packaging material in the US,” says Manu.

Packaging Resources also manufactures plastic containers from recycled bottles. Further, end-users are also using plastic-based foodservice disposables that are manufactured from recycled content. For instance, 30 percent of packaging material used by Dunkin’ Donuts is made from recycled content, and 100 percent of its packaging material is recyclable in nature such as cups, lids, wraps, and trays.

Growing market for biodegradable foodservice disposables

Environment pollution is a major issue for environmentalists and various government agencies. For instance, approximately 40 billion pieces of disposable cutlery, around 115 billion disposable cups, and around 30 billion disposable plates are sold in the US. Many laws and regulations, such as Pollution Prevention Law or P2 Law, have been framed with respect to this. To overcome this issue and reduce the carbon footprint, some manufacturers have started producing disposable products using plant fiber and pulp, which are 100 percent compostable in nature.

GreenGood USA, International Paper, Packnwood, and Sabert are some companies that manufacture disposable products using compostable materials. Similarly, foodservice providers are also focusing on reducing the carbon footprint. McDonald’s, by 2020, aims to operate with 100 percent fiber-based packaging from certified or recycled sources.

Worldwide Cost of Meat

Online catering marketplace, Caterwings, conducted a study regarding the global price of basic food items, as preliminary research ahead of their expansion into foreign markets. The research highlighted in particular that the cost of meat around the world is remarkably varied. To share these insights, Caterwings have released the 2017 Meat Price Index, which details the cost of meat in over 50 countries worldwide. The study revealed that Switzerland has the highest meat prices, at 141.9 percent more expensive than the average cost worldwide, followed by Norway (63.7 percent more expensive) and Hong Kong (61 percent more expensive), while Ukraine has the least expensive meat prices, at 52.3 percent less expensive than the average cost, closely followed by Malaysia (50.3 percent less expensive).

To give some perspective to the data, the affordability of meat in each country was calculated to reveal the relative number of hours a person on minimum wage must work to buy each type of meat. The findings confirmed that not only does the price of meat vary massively from country to country, but there is also an enormous disparity in its accessibility for people all around the world.

To create the Index, Caterwings looked at the top meat producing and consuming countries around the world focusing on beef, chicken, seafood, pork and lamb. After reviewing hundreds of food retailers, the data was compiled by analysing meat prices in these countries’ top cities, which needed to account for at least 25 percent of the total population. The Index is then ranked by the deviation percentage—this shows how comparatively affordable or expensive each meat type is in each country, in comparison to the global average cost.

“What began as a simple catering cost price Index for market research has raised some important questions.” commented Caterwings Managing Director Susannah Belcher. “It is clear that international inequality exists, and as the world begins to rethink the implications of globalisation, this study clearly demonstrates that food prices ought to be on the agenda.”

High Demand for Seafood

Seafood is in higher demand than ever before, with 82 percent of Americans adding salmon, shrimp and tilapia to their lunch and dinner plates. However, they won’t settle for just any seafood. They want to know where it’s coming from and that it was sourced responsibly, according to a June 2017 Cargill Feed4Thought consumer survey.

The survey, which polled more than 1,000 U.S. residents, found that 72 percent of American consumers believe seafood is important to their health and nutrition. Eighty-eight percent of those same consumers are willing to pay more for seafood that is certified as sustainably and responsibly sourced. This especially appeals to the younger generation, with 93 percent of millennials agreeing they are willing to pay more.

“The majority of American consumers believe seafood is important to their health and nutrition, but they also want to have peace of mind as to where it came from – and that’s where we can play an integral role,” said Einar Wathne, president, Cargill Aqua Nutrition. “We are committed to delivering healthy seafood for future generations, and we know we must do this in a way that is responsible and meets consumer preferences.”

“It is important that the seafood industry earns consumer trust,” said Avrim Lazar, convener of the Global Salmon Initiative (GSI). “That’s why we work very hard to meet third party, rigorous certification standards. Consumers deserve independent assurance that the seafood they eat is sustainable and responsibly sourced.”

The survey also found:

- Out of the five seafood options given, 47 percent of Americans prefer shrimp (the majority).

- Eighty-four percent of Americans trust that their seafood is sourced in a safe and responsible way.

- Seventy percent of Americans say where and how their seafood is sourced impacts their purchase decision.

Tech-Savvy Millennials

orderTalk, Inc., released a research report on Millennials and their tech-savvy food ordering habits and views. The report reveals that 79 percent of Millennials (ages 18-34) have ordered takeout via a website or app, which is 29 percent more than the older U.S. adult population (ages 45+).

“While we know that Millennials have grown up with technology and are naturally inclined to use it regularly, the survey results shed light on the level of frustration they feel for lagging restaurant online ordering technology,” said orderTalk CEO Partick Eldon. “This information is something restaurants shouldn’t ignore when evaluating their current online ordering systems.”

To support this, the survey statistics revealed that Millennials are 26 percent more likely to wish it were easier to order takeout digitally than Americans ages 45 and older (70 percent versus 44 percent). The study also reported that 69 percent of Millennials who have ordered takeout digitally have abandoned a digital order, and the most common reason was because the website/app was not functioning properly (35 percent).

“Online food ordering has become a way of life,” noted Eldon. “However, merely having an online ordering presence isn’t enough today. Restaurants must offer customers a brand-integrated, easy-to-use online ordering platform that works seamlessly to meet a discerning consumer demand.”

The research report is the result of a 2017 online survey conducted on behalf of orderTalk by Harris Poll among 2,246 U.S adults.

A wide-ranging analysis of the survey results can be found by downloading the full 2017 orderTalk Online Ordering Usage Report here.

Ice Cream in China

Ice cream remains a popular summertime treat for many and new Mintel research reveals that consumption of the sweet indulgence is on the rise. Today, half (49 percent) of urban Chinese consumers* say they eat ice cream at home as a snack, compared to four in 10 (39 percent) who said the same in 2015. Meanwhile, 39 percent of urban Chinese consumers report eating ice cream as a dessert this year, compared to just over one in four (28 percent) who said the same two years ago.

Overall, the ice cream market in China has seen a decline in retail volume, with a CAGR (Compound Annual Growth Rate) of -1.6 percent between 2014 and 2016. However, the total retail market value is on the rise due to consumers trading up for new formats and flavours.

Better-for-you options are among the more popular premium features; 59 percent of urban Chinese consumers are willing to buy ice cream products that feature a ‘100 percent natural/no additive’ claim, especially among soft-serve ice cream users (68 percent). What’s more, consumers aged 30-39 say they are willing to pay more for ‘100 percent natural/no additive’ products (65 percent compared to 59 percent of consumers overall).

Cheryl Ni, Food and Drink analyst at Mintel said, “Urban Chinese consumers are paying more attention to their health, while still looking for opportunities for indulgence, which should not be compromised. Given the fact that more consumers today are eating ice cream as a snack or a dessert at home compared to previous years, family-size tubs or multipack offerings will have further opportunities. Also, there is scope for ice cream to be positioned as ‘mood food’, allowing consumers—especially the younger generations—the ability to soothe life’s stresses away as they indulge in a treat while paying a premium price for it.”

Meanwhile, declining consumption appears in both retail and non-retail channels. Mintel research indicates that the percentage of ice cream non-users has risen from 4 percent in 2012 to 11 percent in 2017. In all, purchases at retail channels (net) (76 percent) is lower than non-retail channels (net) (93 percent), with the number of urban Chinese consumers who bought ice cream from supermarkets/hypermarkets declining from 85 percent in 2012 to 52 percent in 2017. Similar declines can be seen at grocery retailers, which dropped from 42 percent to 12 percent in the same time period.

All that said, the market has experienced significant growth in online channels, including online brand stores (eg. official store in Tmall), increasing from 3 percent to 16 percent between 2012 and 2017. Mintel research indicates that this growth is driven by high earners** who are more likely to be fans of online channels (23 percent).

“Shopping for ice cream products from online retailers is usually more expensive given the cost of cold chain delivery. However, we are seeing a growing number of imported ice cream brands available in online stores, providing more premium choices for consumers with a higher spending power,” she noted.

More Chinese consumers in tier one cities claim to eat packaged ice cream as a snack during their leisure time, especially those located in Shanghai (57 percent vs 49 percent of consumers overall). On the different occasions for eating ice cream that is made on-the-spot, consumers in Shanghai show a higher interest in this format when they are hanging out (54 percent, compared to a total 47 percent) or when they are craving something sweet (41 percent, compared to a total 34 percent). When it comes to location, ice cream parlours, dessert shops and coffee shops seem to be their favourite spots for eating ice cream.

Finally, it appears that young urban Chinese consumers aged 20-24 are particularly interested in value-added features, such as ‘edible containers that taste good’ (42 percent), ‘customised flavours/shapes’ (35 percent) and ‘innovative packaging’ (33 percent). Products with clean label claims and added nutrition will encourage trading up in this category. In the meantime, healthier versions should not compromise indulgence, especially for tier one Chinese consumers.

“The shift in consumption occasions redefines the ice cream market which is no longer an alternative to a cooling drink, but an indulgent treat that can bring a sense of enjoyment and happiness. Consumers in tier one cities prefer healthy versions of ice cream, but they don’t want to compromise on enjoyment, and this is why manufacturers should optimise recipes to achieve a balance of both,” Ni concluded.

Avocados on the Brain

Tufts University released results of a study linking eating avocados to helping improve cognitive brain function in older adults, news especially relevant to Hispanics who have been found to have the longest life expectancy rate in the U.S.1 Published in the journal Nutrients and supported by the USDA and the Hass Avocado Board, the research tracked how 40 healthy adults ages 50 and over who ate one fresh avocado a day for six months experienced a 25 percent increase in lutein levels in their eyes and significantly improved working memory and problem-solving skills.

Lutein is a type of carotenoid antioxidant, or pigment, commonly found in fruits and vegetables already widely accepted to have a role in preserving eye health and now increasingly thought to have a positive impact on brain health as well. As study participants incorporated one medium avocado into their daily diet, researchers monitored gradual growth in the amount of lutein in their eyes and progressive improvement in cognition skills as measured by tests designed to evaluate memory, processing speed and attention levels. In contrast, the control group which did not eat avocados experienced fewer improvements in cognitive health during the study period.

“The results of this study suggest that the monounsaturated fats, fiber, lutein and other bioactives make avocados particularly effective at enriching neural lutein levels, which may provide benefits for not only eye health, but for brain health,” said Elizabeth Johnson, Ph.D., lead investigator of the study from the Jean Mayer USDA Human Nutrition Research Center on Aging, at Tufts University. “Furthermore, the results of this new research reveal that macular pigment density more than doubled in subjects that consumed fresh avocados, compared to a supplement, as evidenced by my previous published research. Thus, a balanced diet that includes fresh avocados may be an effective strategy for cognitive health.”

“Tuft’s findings that eating avocados is linked to a positive impact on memory is one more reason to enjoy healthy avocados daily. It’s especially good news for Hispanic households where avocados are already so popular and older generations are culturally central to the core family unit,” said Emiliano Escobedo, Executive Director of the Hass Avocado Board. “More research is needed in different populations with different amounts of avocado to better understand the connection between avocados and brain health.”